Smart Cent Guide

Banking & Accounts

Comparisons and guides on financial products, focusing on finding the best high-yield savings accounts, CD rates, and everyday banking options.

Closing Day Step-by-Step

Closing day is one of those calendar squares that looks simple until you are living it. You have a final walkthrough, a mountain of documents, a mysterious “cash to close” number, and a lot of people saying things like “we are waiting on recording.” This guide walks you through the full...

Read more →

401(k), 403(b), and IRA Rollovers: Direct vs Indirect

If you are moving money out of an old 401(k), 403(b), or IRA, the rollover method you choose matters a lot. Do it the clean way and it is usually tax-free and low-stress. Do it the messy way and you can accidentally create a taxable distribution, get hit with a 10% penalty, or lose some of your...

Read more →

HSA-Eligible HDHP in 2026: Rules, Limits, and Mistakes to Avoid

If you are picking a health plan for 2026, the phrase “HSA-eligible” can look like a simple checkbox. In practice, it comes with a rulebook. Your plan has to meet specific IRS requirements for an HDHP, and you also have to avoid a few easy-to-miss coverage gotchas that can make your HSA...

Read more →

Tax-Loss Harvesting and Wash Sale Rules

Tax-loss harvesting sounds fancy, but the idea is simple: if you have investments in a taxable brokerage account that are down, you may be able to sell them at a loss and use that loss to lower your tax bill. The catch is the wash sale rule . It is basically the IRS saying, “You do not get to...

Read more →

FHA Streamline Refinance: No-Appraisal Option, MIP Rules, and When It Pays

If you already have an FHA mortgage and you keep hearing “streamline refinance” tossed around like it’s a magic coupon, here’s the real deal. An FHA Streamline Refinance is designed to lower your monthly payment or move you into a more stable loan with less paperwork than a traditional...

Read more →

ARM vs Fixed-Rate Mortgages in 2026

If you have been mortgage shopping in 2026, you have probably seen two very different pitches: Fixed-rate mortgage: stable principal-and-interest payment, rate does not change. ARM (adjustable-rate mortgage): often a lower starting rate, then your rate (and payment) can change later. And if you are...

Read more →

Appraisal vs Home Inspection: What’s the Difference?

If you are buying a home, the terms appraisal and home inspection can sound like the same thing. They are not. One is about value for the loan. The other is about condition for your peace of mind. Understanding the difference matters because a “bad” inspection can change whether you want the...

Read more →

USDA Home Loans: Income Limits, Property Eligibility, and FHA vs USDA

USDA home loans are one of the most underrated ways to buy a home with no down payment and affordable monthly costs. The catch is that USDA loans are built for specific areas and specific income ranges. If you have ever assumed “rural” means “middle of nowhere,” or you have been scared off...

Read more →

FHA 203(k) Loans in 2026: Renovation Mortgage Rules, Costs, and Alternatives

If you have ever walked into a house and thought, “This place could be amazing… after a new roof, a kitchen, and about twelve trips to Home Depot,” you have already understood the basic problem that FHA 203(k) loans solve. A 203(k) loan is an FHA mortgage that lets you buy (or refinance) a...

Read more →

Mortgage Rate Lock: When to Lock and What Can Go Wrong

A mortgage rate lock can feel like trying to “hit the button” at the perfect second. Lock too early and you might pay more in pricing for a longer lock (via a slightly higher rate, more points, or fewer lender credits). Wait too long and you can get burned by a rate jump right before closing....

Read more →

Loan Estimate vs. Closing Disclosure

If you are buying a home with a mortgage, two documents matter more than almost anything else you will sign: the Loan Estimate (LE) and the Closing Disclosure (CD) . They look similar on purpose, but they do not show up at the same time, and they do not have the same rules for what can change. I am...

Read more →

FHA MIP Explained: Upfront vs Annual, How Long You Pay, and How to Remove It

FHA loans are popular for a reason: flexible credit guidelines, smaller down payments, and a path to homeownership that is realistic for many everyday buyers. The tradeoff is FHA mortgage insurance , also called MIP . If you have been Googling “How do I get rid of FHA MIP?”, you are not alone....

Read more →

Escrow Accounts Explained

If your mortgage payment jumped and your lender blamed “escrow,” you are not alone. Escrow is one of the most confusing parts of homeownership because it affects your monthly cash flow, but it is based on bills you do not directly pay each month: property taxes and homeowners insurance. Quick...

Read more →

Mortgage Preapproval vs Prequalification

If you have been browsing homes for more than five minutes, you have probably heard both phrases: prequalified and preapproved . They sound similar, but they do not carry the same weight with sellers, real estate agents, or even your own budget. Here is the clean way to think about it:...

Read more →

HELOC vs Cash-Out Refinance (2026): Costs, Risks, and Tax Rules

If you have home equity, you have a few levers you can pull when you need cash. Two of the most common are a HELOC (home equity line of credit) and a cash-out refinance . Both let you convert equity into spendable dollars, but they do it in very different ways. And in 2026, those differences matter...

Read more →

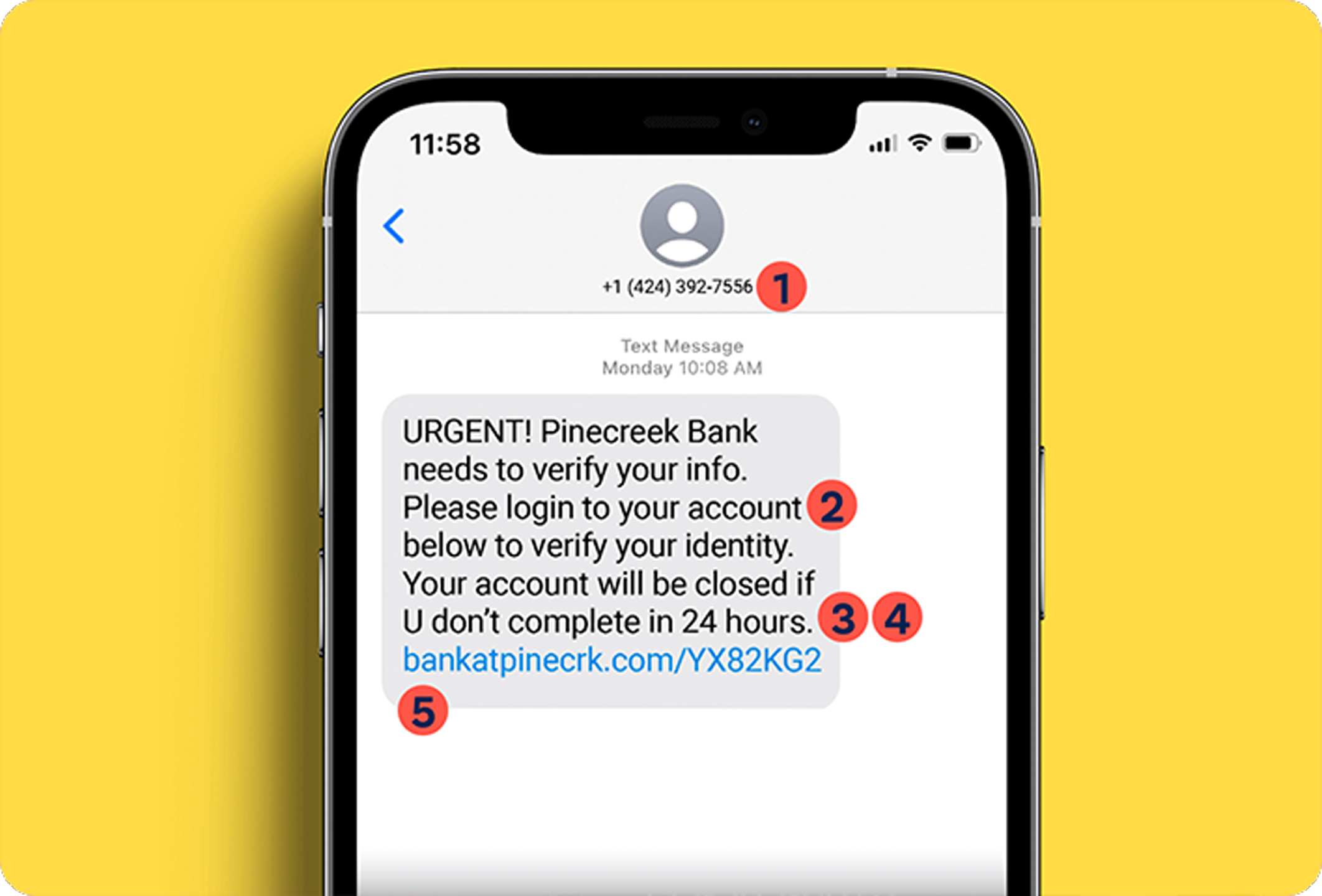

How to Spot a Bank Scam Email or Text

If you have ever gotten a text that says “Fraud alert: confirm this charge now” or an email that claims your account is locked, you are not alone. Scammers copy bank logos, use urgent language, and try to create just enough panic that you click before you think. Here is the simple rule I live...

Read more →

Checking vs Savings Account: What Each Should Be For

If you’ve ever wondered, “Why do I even need two bank accounts?” you’re not alone. When I was digging out of debt, I used to treat my checking account like a catch-all bucket: bills, spending money, random savings, everything. That worked until it didn’t. One unexpected expense, one...

Read more →

Secured Credit Cards vs Credit Builder Loans

If you are trying to build credit from scratch or rebuild after a rough patch, you have probably seen two “safe” options everywhere: secured credit cards and credit builder loans. Both can work. Both can backfire if you pick the wrong product or use it the wrong way. Let’s make this simple: a...

Read more →

Mortgage Points: When Buying Down Your Rate Pays Off

Mortgage points are one of those “sounds smart, feels confusing” line items you will see on a Loan Estimate. And to be fair, points can be a great move. They can also be an expensive way to prepay interest you will never actually owe if you sell or refinance sooner than you think. Let’s make...

Read more →

FHA vs Conventional Loan: What to Compare Beyond the Down Payment

If you are buying your first home, it is tempting to reduce the decision to one headline: FHA is 3.5% down and conventional is 5% to 20% down . Real life is messier. And to be clear, that conventional headline is not always true. Some first-time buyer conventional programs go as low as 3% down . I...

Read more →