If you get a big tax refund every year, it can feel like a win. Often, it is proof you overpaid the IRS a little bit at a time all year long.

Quick exception: some large refunds are driven by refundable credits (like the EITC or Additional Child Tax Credit). In those cases, the refund is not only “your money coming back.” It can be a credit you receive when you file.

I used to do this without realizing it. I thought “bigger refund = smarter money.” Meanwhile, I was stressing about cash flow, juggling bills, and carrying credit card balances that cost way more in interest than my refund was earning.

The fix is usually simple: update your W-4, the form that tells your employer how much federal income tax to withhold from each paycheck.

One important reminder: changing your W-4 generally does not change your total tax bill. It changes when you pay it (through the year vs. at filing time).

What withholding is

Withholding is the prepayment of your federal income tax. Every payday, your employer withholds a portion of your wages and sends it to the IRS on your behalf.

Your goal is not “pay as little as possible.” Your goal is to pay about the right amount across the year so you do not:

- Overpay and wait for a refund you could have used for bills, savings, or debt.

- Underpay and get hit with a surprise balance due, or even penalties in some cases.

The W-4 is how you steer that middle path.

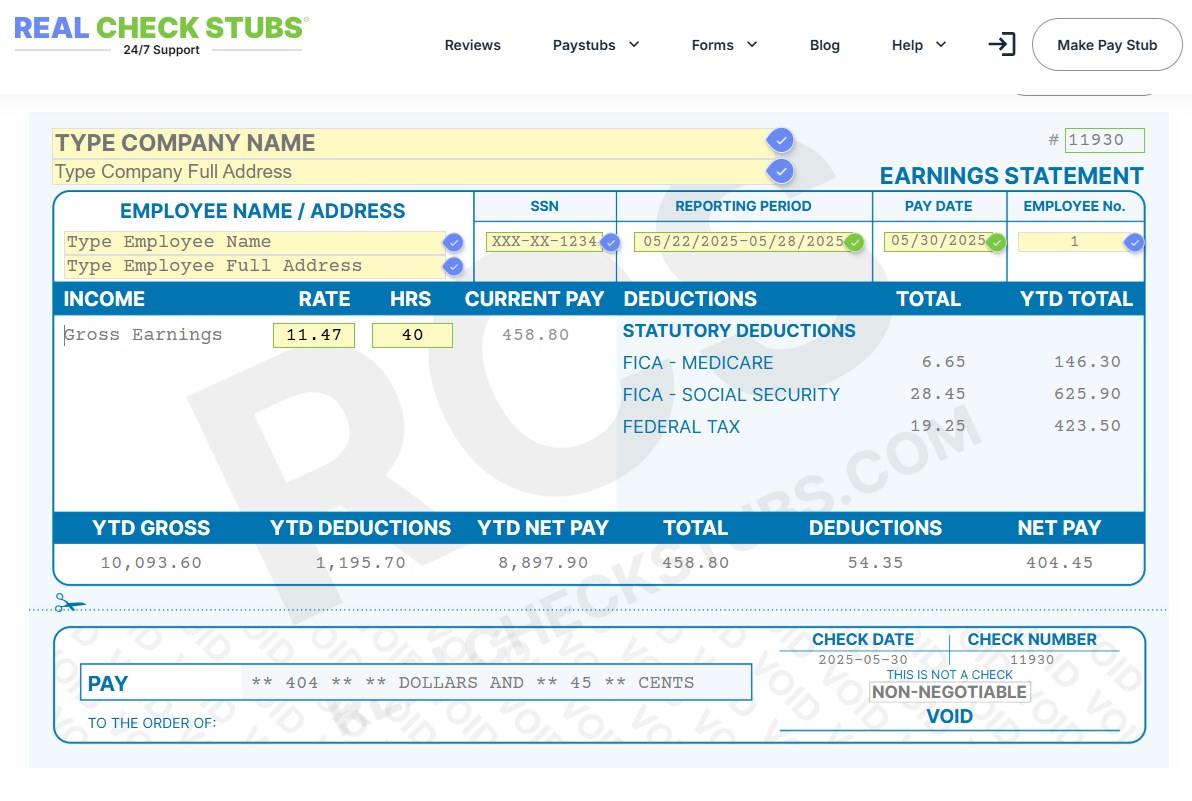

Where to see it on your pay stub

If you have read our paycheck-stub guide , you already know the basics. Here is the quick refresher focused on W-4 decisions.

The lines that matter most

- Gross pay: what you earned before any deductions.

- Pre-tax deductions: things like traditional 401(k) contributions and some health insurance premiums that can reduce taxable income.

- Federal income tax: the line your W-4 mainly affects.

- Social Security and Medicare: separate from income tax and generally not affected by your W-4.

- State and local withholding: usually handled separately (state forms, local forms, or payroll settings), not the federal W-4 itself.

When people say “my taxes are high,” they often lump everything together. For W-4 purposes, you are mostly adjusting the federal income tax line.

How the W-4 works now

Older W-4s used “allowances.” The current W-4 is more direct. You tell payroll about your household situation, and the payroll system uses IRS tables to estimate what you will owe for the year.

The W-4 has a few levers that matter:

Step 1: Filing status

This is where you pick Single, Married filing jointly, or Head of household. This choice changes the baseline withholding calculation.

Step 2: Multiple jobs or spouse works

This is one of the biggest “refund or balance due” trouble spots. If your household has two incomes and you do not account for it, you can end up underwithheld.

The W-4 gives you a few ways to handle this. One is the Step 2(c) checkbox (the “two jobs” box). It tends to work best when there are only two jobs total and the pay is similar. If pay is not similar, or there are more than two jobs, the IRS estimator (or the worksheet) is usually the safer route.

Step 3: Dependents and credits

Instead of allowances, you enter annual dollar amounts tied to credits (like the Child Tax Credit and Other Dependent Credit). These amounts are for the year, not per paycheck. If you qualify, this reduces withholding so you keep more money in each paycheck.

Step 4: Other adjustments

- 4(a) Other income: income you expect that does not have withholding, like interest, dividends, or some side hustle income.

- 4(b) Deductions: if you expect to itemize or have deductions beyond the standard deduction, this can reduce withholding.

- 4(c) Extra withholding: an extra flat dollar amount taken out per paycheck. This is the cleanest, least confusing knob to turn when you need more withheld.

Important: Step 4(c) can only increase withholding. You cannot enter a negative number to reduce withholding. If you are overwithheld and 4(c) is already $0, you typically lower withholding by fixing Step 3 (credits) or Step 4(b) (deductions), or by correcting Step 1 and Step 2.

Why you might be overpaying

Overwithholding happens for a few common reasons. If you recognize yourself in any of these, you are not alone.

- You set your W-4 once and never touched it, even after raises, marriage, kids, or a second job.

- You are filing “Single” out of habit even though your actual filing status is different.

- You claim dependents wrong, or you avoid claiming them because you are afraid of owing.

- You added extra withholding “just in case” (Step 4(c)) and forgot it is there.

- You have pre-tax deductions that grew (like a higher 401(k) contribution), which can lower taxable income and make your withholding too high if you do not update.

The goal is not to squeeze your refund down to $0 exactly. Real life is messy. But if you are consistently getting a very large refund (and it is not mostly refundable credits), it is worth checking.

Using the IRS estimator

The IRS Tax Withholding Estimator is the most straightforward way to dial in your W-4 because it works from your real numbers.

Here is what it does:

- Estimates your total income for the year based on what you have earned so far and what you expect to earn.

- Estimates your tax bill using your filing status, deductions, and credits.

- Compares your estimated tax bill to what has already been withheld from your paychecks.

- Calculates what should be withheld going forward to land near your target refund or near zero due.

- Spits out a W-4 recommendation, often using Step 4(c) extra withholding or other fields to get you on track.

What to gather first

- Your most recent pay stub for each job in the household.

- Year-to-date wages and year-to-date federal withholding (both are on your pay stub).

- Any recent bonus info, if you expect more bonuses this year.

- An estimate of side income, interest, dividends, or rental income.

- Your expected deductions and credits (for most people, standard deduction plus any child-related credits).

If you want the estimator to be meaningful, the year-to-date numbers are the key. That is why paycheck-stub literacy matters so much here.

A safe way to adjust your W-4

Here is the approach I recommend if you are nervous about changing anything. It is slower, but it lowers the odds of an unpleasant April.

1) Choose a target refund

If you typically get a $3,000 refund, you do not need to jump straight to $0. You might aim for $500 to $1,000 as a cushion while you learn how your situation behaves.

2) Make one change at a time

Do not change filing status, dependents, other income, deductions, and extra withholding all at once unless you are following a single estimator result. If you are self-adjusting, change one lever and then observe.

3) Use Step 4(c) for clean fine-tuning when you need more withheld

Step 4(c) extra withholding is the easiest lever to control because it is a simple flat amount per paycheck.

- If you are underwithheld, increasing 4(c) is often the cleanest fix.

- If you are overwithheld and you already have a number in 4(c), lowering it or removing it can help.

- If you are overwithheld and 4(c) is $0, you usually reduce withholding by correcting Step 1 or Step 2, claiming the right credits in Step 3, or using Step 4(b) if you truly expect higher deductions.

4) Re-check after 1 to 2 paychecks

After the change hits payroll, compare:

- New federal income tax withheld per paycheck

- Your take-home pay change

- Whether anything else changed unexpectedly (benefits, retirement contributions, etc.)

5) Do a mid-year check-in

I like a quick check in late spring or early summer, and again in early fall if income is variable. If you have a bonus-heavy job or big side hustle swings, check more often.

Quick pace check

You do not need to be a tax pro to do a simple “pace” check.

Step-by-step pace check

- Find your year-to-date federal income tax withheld on your pay stub.

- Estimate how many paychecks you get in a year (26 biweekly, 24 semi-monthly, 12 monthly, etc.).

- Estimate how many paychecks have already happened.

- Project your annual withholding: (YTD withholding ÷ paychecks so far) × total paychecks.

Then compare that rough annual withholding estimate to last year’s total tax number on your tax return. If your income is similar this year, you will quickly see whether you are trending toward overpaying or underpaying.

Note: withholding is not perfectly linear. A bonus, a job change, or updated payroll tables can make your pace jump around. This check is meant to be a quick early warning system, not a final answer.

Situations to watch

Two-income households

This is the big one. With two jobs, each employer withholds as if that job is the only income unless you tell them otherwise. That can cause underwithholding, but sometimes people overcorrect and end up overwithholding. The estimator is your friend here.

Bonuses and commission

Bonuses are often withheld at a flat federal rate under one common payroll method, but some employers use a different method that treats the bonus like regular wages. If you get big bonuses, do a check after a bonus hits.

Side hustle or 1099 income

If you have meaningful income that is not run through W-2 payroll (like 1099 work), your W-4 only helps indirectly. You can cover the tax in two common ways:

- Add extra withholding on your W-4 Step 4(c), or

- Pay quarterly estimated taxes.

Many people prefer extra withholding because it is automatic and feels simpler. But if most of your income is self-employed, estimated payments may be the more direct tool.

New baby or newly claiming a child

Credits can reduce your overall tax bill. If you qualify and you do not update your W-4, you may overwithhold and get a big refund later.

Marriage or divorce

Your filing status and household income picture can change overnight. Update the W-4 sooner rather than waiting for tax season.

How to update your W-4

Most employers let you update your W-4 through an HR portal. Some will have you fill out a paper form.

Tips that make this smoother:

- Confirm when changes take effect. Some companies update immediately, others take one or two payroll cycles.

- Save a copy of what you submitted.

- Check your next pay stub to confirm the federal withholding line changed as expected.

Guardrails

Most people are not trying to game the system. They just want their paycheck to reflect reality. These guardrails help you adjust responsibly.

Leave a buffer for variable income

If you work overtime, get commissions, or have variable side income, aim for a modest refund instead of cutting it too close.

Do not ignore state taxes

This article focuses on the federal W-4, but state withholding can be its own source of surprises. If your state uses a separate form, review it too, especially after life changes.

Be careful with “exempt”

Marking yourself exempt from withholding when you do not qualify can create a big tax bill. If you are unsure, skip that route and use normal adjustments instead.

Know the safe harbor basics

Penalties are not just about owing at filing time. At a high level, many taxpayers can avoid underpayment penalties if they pay in enough during the year, commonly by meeting a safe harbor such as paying around 90% of the current year tax or 100% of the prior year tax (higher-income households may have a higher prior-year threshold). If you are making a big withholding change, this is why a little cushion is smart.

If you started the year underwithheld, you may need to catch up

Sometimes the estimator recommends extra withholding for the rest of the year to make up for a shortfall. That can feel annoying, but it is better than getting blindsided at filing time.

My value-spender take

I am a “value-spender,” meaning I spend intentionally on what I value and cut the rest.

If fixing your W-4 gives you an extra $50 to $300 per paycheck, that money can disappear fast unless you give it a job.

Here are high-impact places to send it:

- High-yield savings for your emergency fund.

- High-interest debt (especially credit cards).

- Sinking funds for predictable expenses like car repairs, travel, or back-to-school shopping.

- Retirement contributions if you are already stable on cash flow.

The point is to keep more of your money working for you now, instead of waiting for a refund later.

FAQ

Is a big refund always bad?

No. Some people like the forced savings. And some refunds are largely refundable credits, not overwithholding. But if you are carrying high-interest debt, skipping savings, or stressing about bills, a huge refund is usually a sign your money could help you more during the year.

Can I change my W-4 anytime?

In most jobs, yes. You can submit an updated W-4 whenever your situation changes or when you want to adjust.

How fast will my paycheck change?

Typically within 1 to 2 payroll cycles, depending on your employer’s processing timeline.

Should I use Step 4(a) and 4(b)?

Only if you are confident in your numbers. If you want a simpler path, many people can get close using filing status, Step 2, Step 3 credits, and Step 4(c) when needed, especially when paired with the estimator.

Bottom line

Your W-4 is not a one-time form. It is a tool. If you are overpaying taxes every paycheck, you can often fix it in under 30 minutes by reviewing your pay stub, using the IRS estimator with your real year-to-date numbers, and making a cautious adjustment.

If you want the simplest next step, pull up your latest pay stub and find your year-to-date federal withholding. That one number tells you a lot about whether your refund is being built one paycheck at a time.