If you just inherited a retirement account, first off, I am sorry for your loss. Second, take a breath. The rules can feel like they were written to make you panic-Google at midnight.

The big headline in the SECURE Act era is this: many beneficiaries have to empty an inherited retirement account within 10 years. But the details depend on who you are, what you inherited, and whether the original owner had started required minimum distributions (RMDs).

Step 0: Get the account titled correctly

Before you move money, make sure the inherited account is set up and titled properly. This is usually something like: [Decedent Name] IRA FBO [Your Name].

Do not take a distribution from the original account first and hope to sort it out later. A clean, correctly titled inherited IRA (or inherited plan account) is what keeps your options and your paperwork intact.

The 10-year rule in plain English

The 10-year rule means that certain beneficiaries must withdraw the entire balance of an inherited retirement account by the end of the 10th year after the account owner died.

What it does and does not require

- It does require the account to be fully emptied by the deadline.

- It may require withdrawals in some years along the way, depending on the situation.

- It does not automatically require equal withdrawals every year.

Think of it like a 10-year window that eventually slams shut. You can take money earlier, later, or spread it out, as long as you follow any annual requirements that apply to your case and the account hits zero by the end.

Who is subject to the 10-year rule?

In general, the 10-year rule applies to many non-spouse beneficiaries who inherit after the SECURE Act changes (for most people, that is deaths in 2020 or later).

The most common people who land in the 10-year bucket:

- Adult children

- Grandchildren

- Siblings

- Unmarried partners

- Friends or other non-spouse individuals

- Most non-eligible trusts named as beneficiaries

If that describes you, your next step is figuring out whether you also have to take annual RMDs during the 10-year window. That is where a lot of confusion lives.

A quick glossary: designated vs non-designated

Most of this article is about designated beneficiaries, which generally means an individual person (and certain qualifying trusts) named on the beneficiary form.

- Designated beneficiary: Usually an individual. Often eligible for the 10-year rule (or, if an eligible designated beneficiary, possibly life expectancy payouts).

- Non-designated beneficiary: Often an estate, charity, or a trust that does not qualify as a see-through trust. These can follow different distribution rules than the 10-year framework.

If an estate or charity is involved, pause and get advice. The distribution timing can change, and the “10-year rule” may not be the right mental model.

Spouse vs non-spouse

Spouses typically get more flexibility than everyone else. If you inherited from your spouse, you may have choices that can reduce taxes and simplify life.

If you inherited as a spouse

Spouses may be able to:

- Roll the account into their own IRA (often called a spousal rollover), which can allow normal owner rules going forward.

- Treat it as their own in certain cases, depending on the type of account.

- Remain as a beneficiary using an inherited IRA, which can make sense if you need access before age 59 and a half and want to avoid the 10% early withdrawal penalty that can apply to your own IRA distributions.

Spousal options are powerful because they can shift you back into “owner rules,” which may mean a longer timeline and different RMD timing.

If you inherited as a non-spouse

Most non-spouse beneficiaries cannot roll the account into their own IRA. Instead, they typically use an inherited IRA (or an inherited plan account) and follow beneficiary distribution rules, which often means the 10-year rule.

Key exceptions: eligible designated beneficiaries

Not everyone is stuck with the 10-year deadline. The SECURE Act created a special group called eligible designated beneficiaries (EDBs) who may be able to stretch distributions longer than 10 years (often using life expectancy rules).

EDBs generally include:

- A surviving spouse

- A minor child of the account owner (not a grandchild). Note: once the child reaches the age of majority, the 10-year rule typically kicks in.

- A disabled individual (as defined under IRS rules)

- A chronically ill individual

- Someone not more than 10 years younger than the person who died (often a sibling or partner close in age)

One extra clarification on minors: “age of majority” is generally based on state law, but there are special rules that can extend this in certain cases (for example, some education-related exceptions). This is an area where a quick confirmation can save you from a messy mistake later.

EDB rules can be nuanced, especially for minors and trusts. If you think you might qualify, it is worth confirming with the custodian and a tax pro before you move money.

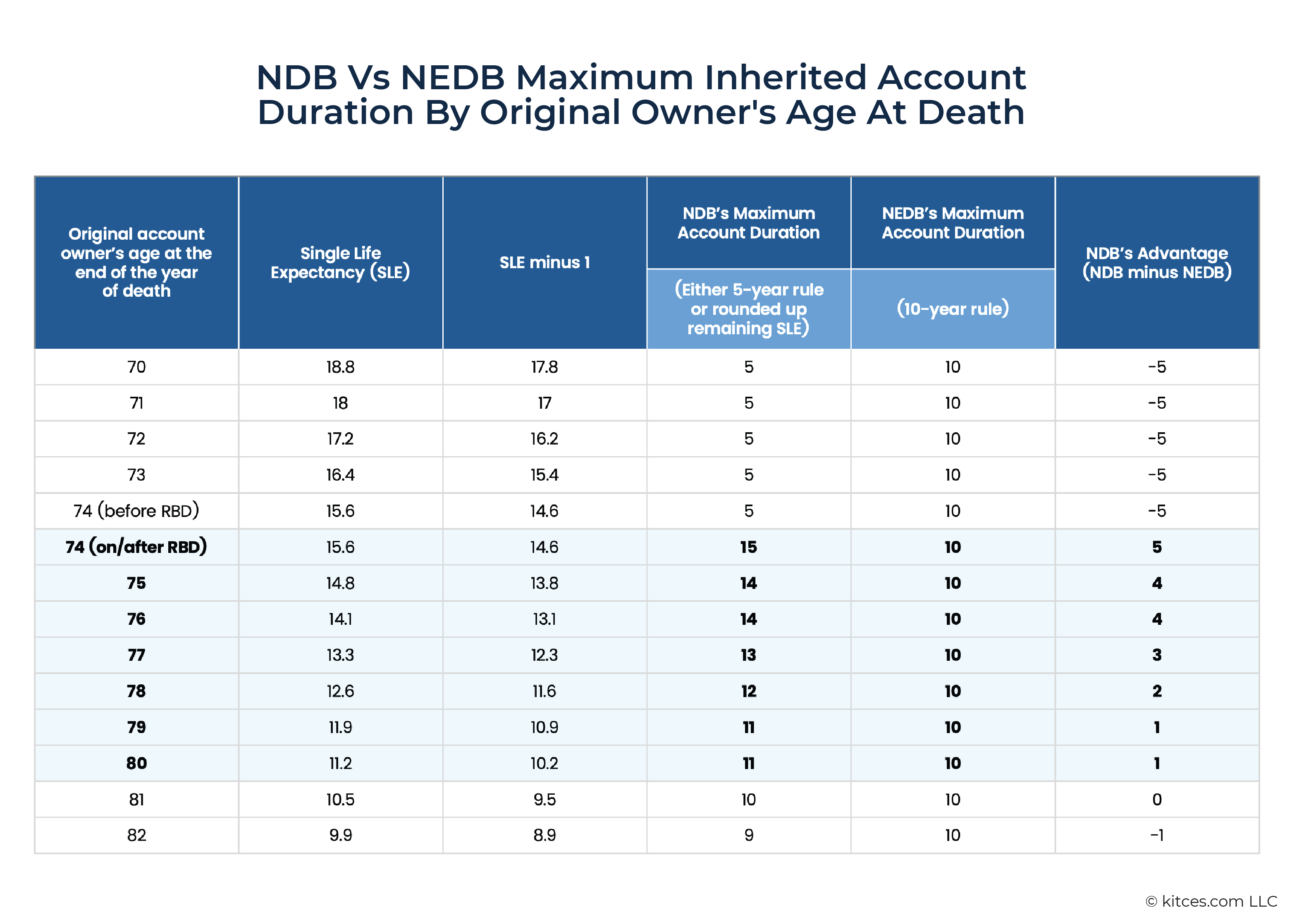

Why RMD timing matters

Here is the part that creates the most “Wait, what?” moments: some beneficiaries under the 10-year rule still need to take annual RMDs in years 1 through 9.

Did the original owner start RMDs?

A common way this is framed is whether the person who died was already required to be taking RMDs (sometimes described as dying on or after their “required beginning date”).

- If the owner died before they had to start RMDs, most designated beneficiaries who are subject to the 10-year rule can often wait and take distributions any way they want, as long as the account is emptied by the end of year 10.

- If the owner died on or after RMDs had begun, then under IRS and Treasury final RMD regulations issued in 2024, most designated beneficiaries subject to the 10-year rule are generally required to take annual distributions in years 1 through 9 and still empty the account by the end of year 10.

Two important caveats:

- EDBs who are using life expectancy payouts are not following the standard 10-year schedule in the same way.

- Some trust and non-designated beneficiary situations can follow different rules entirely.

In other words, the 10-year rule is not always “wait until year 10 if you feel like it.” If you are a non-spouse designated beneficiary and the original owner had started RMDs, assume annual RMDs apply until you confirm otherwise.

Do not assume your bank or brokerage automatically got your exact situation right. Ask specifically: “Do I have annual RMDs under the 10-year rule for this inherited account?”

Why it matters in real life

- Penalty risk: Missing a required distribution can trigger an excise tax. Under the current framework, it is generally 25% of the missed amount, and it can be reduced to 10% if corrected in time. The point is that “oops” can be expensive.

- Tax planning: Waiting until year 10 to take everything could push you into a higher tax bracket, spike your Medicare premiums later, or affect tax credits.

- Withholding surprises: Inherited plan distributions sometimes default to certain withholding rules, so you may need to adjust to avoid a tax bill.

Inherited IRA vs inherited Roth

The 10-year clock can apply to both inherited traditional accounts and inherited Roth accounts. The big difference is how withdrawals are taxed, and whether annual RMDs are part of your life.

Inherited traditional IRA or pre-tax 401(k)

Distributions are generally taxable as ordinary income. This is where spreading withdrawals across years can help keep taxes more manageable.

Inherited Roth IRA (and Roth 401(k))

Qualified Roth distributions are generally tax-free, but you still may have to follow the 10-year empty-the-account rule.

Here is a key detail people miss: because original Roth IRA owners are not subject to lifetime RMDs, beneficiaries of an inherited Roth IRA who are under the 10-year rule generally do not have to take annual RMDs in years 1 through 9. They typically just need to make sure the account is emptied by the end of year 10.

For Roth 401(k) and other Roth employer plans, the practical outcome is often similar today, but plan rules and rollover choices can affect how things play out. If you inherit a Roth 401(k), ask the plan administrator what distribution schedule applies and whether you can move it to an inherited Roth IRA.

Also watch the Roth 5-year rule. If the original owner had not met the 5-year aging period for qualified Roth distributions, earnings may be taxable. For beneficiaries, these withdrawals are typically not subject to the 10% early distribution penalty, but taxes can still apply.

What the 10-year deadline means

The deadline is usually measured to the end of the calendar year.

Example: If the account owner died in 2026, year 1 is 2027, and the account generally must be fully distributed by December 31, 2036.

Two practical notes:

- Year-of-death RMD: If the person who died had an RMD due for the year they died and had not taken it yet, someone usually needs to take it. This is separate from your 10-year strategy.

- Do not wait for December: Custodians get slammed late in the year. If you are taking a year-10 withdrawal, give yourself a buffer.

Smart ways to handle withdrawals

I love a color-coded spreadsheet as much as the next personal finance nerd, but you do not need a 14-tab workbook to make a good plan. You just need a few simple checkpoints.

1) Identify the account type and tax status

- Traditional IRA, 401(k), 403(b) typically mean taxable income.

- Roth IRA or Roth 401(k) may be tax-free, assuming rules are met.

2) Confirm whether annual RMDs apply to you

Ask the custodian directly, and if the answer is fuzzy, verify with a CPA or enrolled agent. This one detail changes everything.

3) Choose a withdrawal rhythm that matches your income

- Stable income: Consider leveling withdrawals to avoid bracket jumps.

- Income likely to rise: Taking more earlier can reduce taxes later.

- Income likely to fall: Waiting for lower-income years can help, assuming you are not required to take annual RMDs.

4) Set aside money for taxes if needed

If you take $20,000 from an inherited traditional IRA, it is not “free money.” Consider withholding or moving a chunk into a high-yield savings account so April does not punch you in the face.

Special situations

Trusts as beneficiaries

Trust rules can get complicated fast. Whether the trust qualifies as a see-through trust and how beneficiaries are defined can affect whether the 10-year rule applies and how distributions work. If a trust is involved, get professional help before moving money.

Inherited employer plans

Some employer plans require you to take distributions faster than an inherited IRA would. In many cases, you can do a direct trustee-to-trustee rollover to an inherited IRA to keep options open, but not every plan allows every move.

Important detail: non-spouse beneficiaries generally cannot roll an inherited employer plan into their own IRA. If a rollover is allowed, it typically has to go into an inherited IRA (or inherited Roth IRA) set up in the proper beneficiary format.

Ask the plan administrator what is permitted for non-spouse beneficiaries.

Multiple beneficiaries

If you and siblings inherit the same IRA, separate inherited IRA accounts may be needed to preserve certain options and simplify RMD calculations. Timing matters, so do not sit on this.

A quick checklist

- Get the death date and confirm the beneficiary designation on file.

- Set up the inherited account with correct titling before taking distributions.

- Ask if a year-of-death RMD is required and whether it was already taken.

- Confirm your beneficiary category: spouse, eligible designated beneficiary, designated beneficiary, or non-designated beneficiary (estate or charity).

- Ask whether annual RMDs apply under the 10-year rule for your situation.

- Decide on a tax strategy for withdrawals, especially for pre-tax accounts.

- Set reminders for any annual distribution requirements and the year-10 deadline.

When to call a pro

You do not need a financial planner for every money move, but inherited retirement accounts are one of the times professional advice can pay for itself.

Consider getting help if:

- You inherited more than one account type (traditional and Roth, or IRA and 401(k)).

- You are in a high tax bracket or expect income swings.

- An estate, charity, or trust is involved.

- You are not sure whether annual RMDs apply to you.

- You want to coordinate distributions with charitable giving or a larger estate plan.

Bottom line: The 10-year rule is simple at the headline level, but the best outcome depends on the details. The goal is not to withdraw as fast as possible. The goal is to withdraw on purpose, on time, and with the least tax stress you can manage.

Sources and further reading

- IRS, Retirement topics: Beneficiary

- IRS Publication 590-B, Distributions from Individual Retirement Arrangements (IRAs)

- SECURE Act (Setting Every Community Up for Retirement Enhancement Act of 2019), Division O of Pub. L. 116-94

- Treasury and IRS final regulations on RMDs under the SECURE Act (issued 2024; see Federal Register and Treasury Decision for the final rule text)