If you have ever had a credit card settled for less than you owed, a medical bill wiped out, or a student loan forgiven, you have probably heard the scary phrase “canceled debt is taxable.” And sometimes it is.

But here’s the part that gets lost in the panic: the IRS has several big exceptions, and many student-loan forgiveness programs are treated differently than credit card or personal loan debt.

In this guide, I’ll walk you through what a 1099-C really means, when forgiven debt counts as taxable income, the most common exceptions (especially insolvency), and what to do if you receive a form in the mail that makes your stomach drop.

What canceled debt means

When a lender forgives, cancels, or discharges a debt, you no longer have to repay that amount. From the IRS’s perspective, that can look like you received a financial benefit similar to income.

This is commonly called cancellation of debt (COD) income. If it’s taxable, you typically report it as income on your federal return.

Common situations that can create COD income

- Settling a credit card for less than the full balance

- Debt management or negotiation where part of the balance is forgiven

- Foreclosure or a lender forgiving a deficiency balance (this gets complicated fast)

- Repossession with a remaining balance that gets written off

- Private student loan settlement or cancellation

- Some student loan forgiveness programs, depending on the type and timing

Important: just because a lender “writes off” a debt on their books does not automatically mean it was legally forgiven or that collection must stop. And even a 1099-C is not always proof that the debt is gone for all purposes. (I’ll cover the collection twist later.)

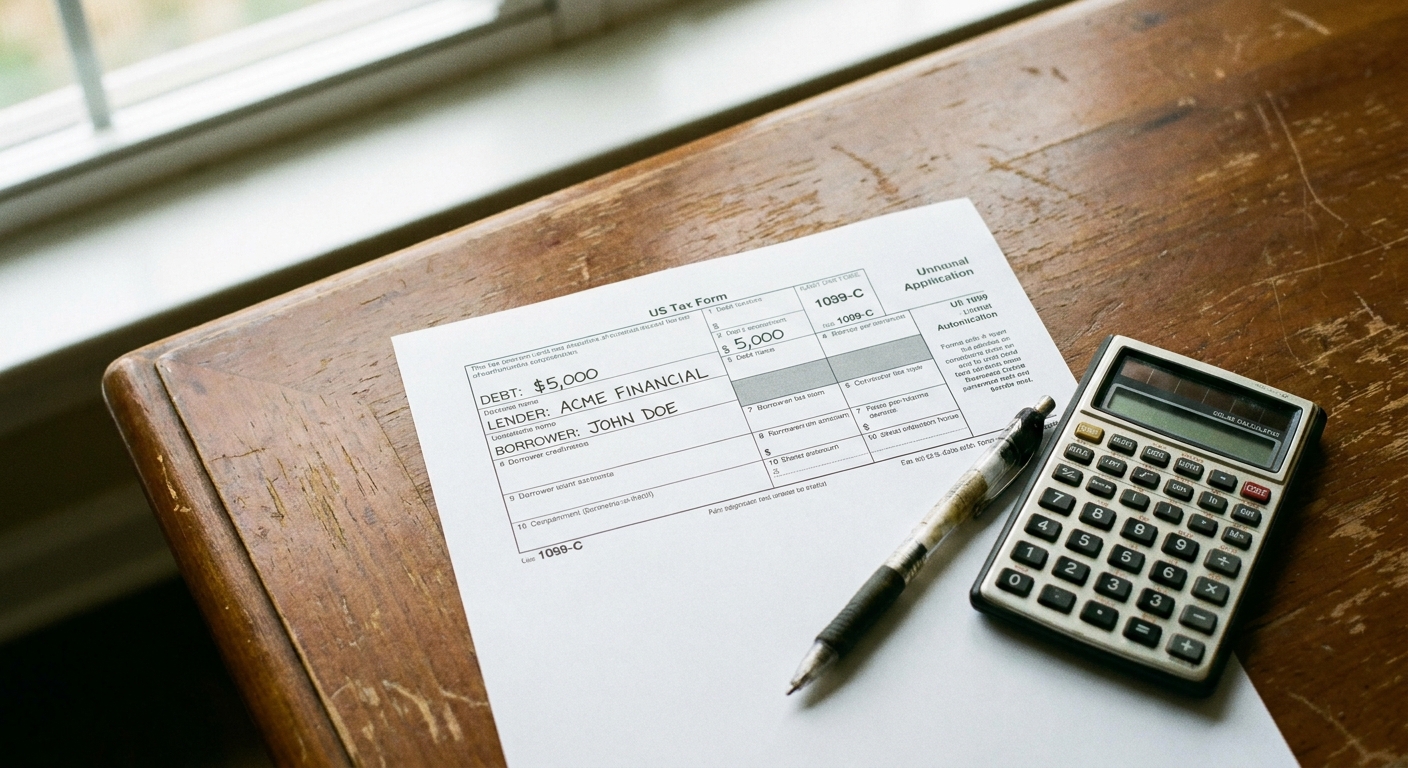

What a 1099-C means

Form 1099-C (Cancellation of Debt) is a tax form a lender may send you (and the IRS) when they cancel a debt of $600 or more.

Two clarifications that save people a lot of confusion:

- The $600 threshold is mainly an issuer reporting rule. If a lender is required to file, they generally must provide you a copy. Some situations and entities have different reporting rules.

- You can still have taxable COD income even without receiving a 1099-C. So if you know a debt was forgiven, it may still need to be addressed on your return.

In plain English: it’s the lender saying, “We’re reporting a cancellation-related event and an amount.”

Key boxes to check on a 1099-C

Box numbers can vary a bit by year, so always read the labels on your form. On the current standard Form 1099-C:

- Box 1: Date of identifiable event

- Box 2: Amount of debt discharged

- Box 3: Interest included (if any)

- Box 6: Identifiable event code (letter code for why they issued it)

- Box 7: Fair market value of property (often relevant for foreclosures)

If you got a 1099-C, do not ignore it. The IRS likely received the same form, and mismatches can trigger letters later.

When canceled debt is taxable

In many everyday cases, canceled debt is taxable. For example:

- You owe $10,000 on a credit card.

- You settle it for $6,000.

- The creditor forgives $4,000.

That $4,000 is often treated as taxable COD income unless an exception applies.

It can feel unfair, especially if you were struggling. But remember: the IRS is basically saying you received a $4,000 benefit you did not have to repay.

Where COD income is reported

If the canceled amount is taxable, it is generally reported as other income on your federal return (often flowing through Schedule 1, depending on your filing situation and tax software).

If you qualify for an exclusion (like insolvency or bankruptcy), you typically claim it using IRS Form 982. In a practical sense, Form 982 is what tells the IRS, “Yes, there was canceled debt, but all or part of it is excluded from income.”

Exceptions that can make it not taxable

This is where most people find relief. The tax code includes several situations where canceled debt can be excluded from income.

1) Insolvency exclusion

You may be able to exclude canceled debt from taxable income if you were insolvent right before the debt was canceled.

Insolvent means your total debts were greater than your total assets.

Example (simple numbers):

- Total debts: $45,000

- Total assets (cash, car value, retirement accounts, etc.): $30,000

- You are insolvent by $15,000

If $8,000 of debt is canceled and you were insolvent by $15,000, you can often exclude the entire $8,000. If $20,000 is canceled, you may be able to exclude only up to $15,000, with the remaining $5,000 potentially taxable.

To claim this, you generally file IRS Form 982 with your tax return.

2) Bankruptcy discharge

Debt discharged in a Title 11 bankruptcy is generally not taxable.

This is also typically handled through Form 982.

3) Mortgage debt relief (situational)

Home-related cancellations can be treated differently depending on the year and your situation. You may see references to rules for qualified principal residence indebtedness, and availability depends on tax year and eligibility.

Also, foreclosure-related tax issues can involve more than COD income. Depending on recourse vs nonrecourse debt and how the property was used, there may also be sale/transfer tax concepts in play (gain, loss, and basis). If your 1099-C involves a foreclosure, short sale, or mortgage deficiency, it is smart to get tax help because the treatment can hinge on details.

4) Gifts and other narrow exclusions

In some cases, canceled debt can be treated as a gift or qualify for other narrow exclusions. These are less common for typical lender situations, but they exist.

Student loan forgiveness taxes

This is the part that intersects with a lot of student-loan conversations on Smart Cent Guide. Not all forgiveness is created equal, and the tax treatment depends heavily on the program and the year.

PSLF

PSLF forgiveness is not taxable at the federal level under current law. So if you have your remaining Direct Loan balance forgiven after making qualifying payments while working for an eligible employer, you should not have a federal “tax bomb” from that forgiveness.

That said, always double-check your state rules. Federal treatment and state treatment can differ.

IDR forgiveness

IDR plans can forgive remaining balances after you meet the required repayment period. Historically, that forgiveness could be taxable federally.

However, under the American Rescue Plan Act (ARPA), many student loan discharges are excluded from federal taxable income for tax years 2021 through 2025.

Practical takeaway, especially now that we are looking at 2026 and beyond:

- If your forgiveness happens in 2021–2025, it may be federally tax-free under ARPA (assuming it fits within the ARPA rules and no exception applies).

- If your forgiveness happens in 2026 or later, you should plan for the possibility that it is taxable again unless the law is extended or changed.

- State taxes are a separate question, and state conformity varies.

If you have read our PSLF content and are comparing it to IDR, this tax difference can be one of the biggest real-world planning points.

Borrower Defense, disability, and school closure

Some types of federal student loan discharge may be excluded from taxable income, depending on the program rules and the year. These programs also come with their own documentation requirements. If you receive paperwork showing a discharge, save everything and confirm whether you should expect a tax form.

Private student loan settlements

Private lenders that settle or cancel part of your balance are more likely to treat the forgiven amount like typical canceled consumer debt. That can mean a 1099-C and potentially taxable COD income unless an exception like insolvency applies.

1099-C and interest

If your 1099-C shows an amount in Box 3 (interest included), it means the lender is saying part of the discharged amount was interest.

How that affects you depends on your situation. For many consumers, the simplest rule of thumb is this: you do not get to claim a deduction for personal interest in the first place, so interest showing up on the form does not automatically create a tax “benefit” to offset it. If the canceled debt is taxable and no exclusion applies, the amount reported can still increase taxable income. If you are using the insolvency or bankruptcy exclusion, Form 982 is often the key step that prevents that reported amount from becoming taxable.

If the numbers feel off, or the interest treatment is confusing in your case, this is a great place to ask a CPA or enrolled agent for a quick check.

What to do if you receive a 1099-C

If you opened your mail and found a 1099-C, take a breath. Then do this:

- Confirm it’s accurate. Compare the lender name and account info to your records. Check the amount. If anything looks wrong, contact the issuer and document every call.

- Identify the debt type. Credit card settlement, repossession, mortgage, private student loan, medical debt. The category matters.

- Use the right date for timing. For many issues (including the insolvency snapshot), the key timing is typically right before the “identifiable event” date shown on the 1099-C. Settlement paperwork and the 1099-C date do not always line up, so do not assume.

- Check for exceptions. Was this debt discharged in bankruptcy? Were you insolvent right before the cancellation event? Was it tied to a program that is federally tax-free in that year?

- Calculate insolvency if applicable. Make a list of your assets and debts as of the day before the identifiable event date. Use realistic fair market values and include all liabilities.

- File the right forms. If you are excluding the canceled debt due to insolvency or bankruptcy, you generally use Form 982. Most tax software can walk you through this, but it helps to know the form name.

- Consider professional help. If the amount is large, involves a house, or you are unsure about insolvency math, a CPA or enrolled agent can be worth it. One hour of paid advice can prevent a multi-thousand-dollar mistake.

Pro tip from someone who has lived in debt math for years: put the 1099-C in a folder with your settlement agreement or discharge paperwork. If the IRS ever asks questions, having everything in one place reduces stress a lot.

Insolvency basics

Insolvency sounds technical, but the concept is simple: what you owe versus what you own.

Assets commonly included

- Cash in checking and savings

- Car value (approximate fair market value)

- Home value (fair market value)

- Retirement accounts (yes, typically included in the insolvency worksheet)

- Investments

- Other property with meaningful value

Debts commonly included

- Credit cards

- Student loans

- Auto loans

- Mortgages

- Medical debt

- Personal loans

- Collections accounts

Common insolvency mistakes

- Using what you paid instead of fair market value for assets (cars and homes are the big ones).

- Forgetting retirement accounts because they are “off limits” in your mind. The worksheet often includes them anyway.

- Leaving out liabilities (especially smaller cards, collections, or personal loans).

- Mixing up shared finances. Married filing status and jointly owned assets or debts can make the calculation less straightforward.

If you are close to the line, this is where a tax pro can help you avoid under or over-reporting. The IRS provides an insolvency worksheet in guidance related to canceled debt, and many tax tools mirror it.

Will forgiven debt always come with a 1099-C?

Not always. Some forgiveness programs do not use 1099-C in the same way, and sometimes canceled amounts under $600 are not required to be reported on that specific form.

Also, there are cases where a creditor may issue a 1099-C even though you later see collection attempts for the same debt. The rules around “identifiable events” can be confusing, and practices vary. If you receive a 1099-C and later get collection attempts for the same debt, do not assume it is automatically invalid. Document everything and consider getting legal or tax guidance depending on the amount.

PSLF vs IDR planning

If you are weighing PSLF versus an IDR path that ends in forgiveness, taxes belong in the plan.

- PSLF: generally no federal tax on the forgiven balance, so your strategy is mostly about eligibility and staying compliant.

- IDR forgiveness: may or may not be federally tax-free depending on the year and rules in effect. If your timeline points to 2026 or later, it is smart to keep a tax-bill savings plan in your back pocket unless the law changes.

The goal is the same either way: no surprises. Forgiveness should feel like relief, not like a new bill you did not see coming.

Quick FAQs

If my debt is forgiven, do I automatically owe taxes?

No. Canceled debt is often taxable, but major exceptions include insolvency and bankruptcy. Some student loan forgiveness programs are also treated differently, and timing matters.

How much tax will I owe on a 1099-C?

If it is taxable, it is usually treated like ordinary income, meaning the tax depends on your overall income and tax bracket. It is not a flat percentage.

What if I never received the 1099-C but the IRS did?

This happens. Update your address with creditors when possible, and if you suspect a cancellation occurred, pull your IRS transcript or watch for IRS notices. If you get a notice, respond promptly and request a copy of the form from the issuer.

Do states tax forgiven debt the same way as the IRS?

Not always. Federal rules and state rules can differ, including for student loan forgiveness. Check your state’s guidance or ask a tax professional if the amount is significant.

A simple next step

If you are expecting forgiveness or you just received a 1099-C, here’s a low-stress move that helps either way: run an insolvency snapshot (assets vs debts) for the day before the identifiable event date and save it as a PDF. Even if you do not end up needing it, it gives you clarity and a paper trail.

And if you are on a student loan path like PSLF or IDR, build your plan around what you can control: track your paperwork, keep your income documentation organized, and set aside cash if there is any chance your forgiveness could be taxable in your situation.

Friendly reminder: I’m not a tax professional, and this is general education, not individualized tax advice. If your canceled amount is large, your situation involves a home, or you are unsure about insolvency, it’s worth getting help from a qualified tax pro.