If you are charitably inclined and you have money sitting in a traditional IRA, a Qualified Charitable Distribution (QCD) can be one of the cleanest tax moves available in retirement.

In plain English: a QCD lets you send money directly from your IRA to an eligible charity, and that amount can stay out of your taxable income. For many retirees, that is even better than a normal charitable deduction because it can help keep your adjusted gross income (AGI) lower, which can ripple into things like Medicare premiums and how much of your Social Security is taxable.

What a QCD is (and why people love it)

A QCD is a distribution from an IRA that goes straight to a qualifying 501(c)(3) charity. When it is done correctly, the distributed amount is excluded from your income on your tax return.

This matters because many retirees do not itemize deductions anymore. If you take the standard deduction, a normal cash donation might not reduce your taxes at all. A QCD can still deliver a tax benefit because it works by lowering taxable income rather than relying on itemizing.

Common reasons QCDs are so useful

- Lower taxable income without needing to itemize deductions.

- Can count toward your RMD once you are required to take one.

- May help with Medicare IRMAA and Social Security taxation by keeping AGI and modified AGI lower.

- Simple giving if you already donate every year.

Who qualifies in 2026: the age 70½ rule

To make a QCD, you must be age 70½ or older on the date the distribution leaves the IRA.

That “half year” detail is a big deal. You do not have to wait until age 72 or 73 when required minimum distributions (RMDs) usually begin under current law. QCD eligibility starts earlier.

Quick timeline that helps people keep this straight

- QCD eligibility: begins at age 70½.

- RMD age: generally begins later (depending on your birth year), but QCDs can still be used before your first RMD year.

Important: QCDs are typically made from traditional IRAs and inherited IRAs (assuming the inherited IRA rules and your situation allow a distribution). QCDs are not available from an active employer plan like a 401(k) unless you first roll money into an IRA.

2026 annual limit: how much you can QCD

The QCD limit is indexed for inflation under SECURE 2.0, so it has been rising in recent years. It was $105,000 in 2024 and $108,000 in 2025.

For 2026, expect the annual QCD limit to be higher than $108,000 per person (the exact number can change, so confirm the official IRS figure for the year you give).

A few practical points people miss:

- The limit is per taxpayer, not per IRA. If you have three IRAs, your combined QCD total is still capped.

- For married couples, each spouse with their own IRA can do their own QCD up to the annual limit.

- The limit applies to the total of all QCDs you do during the calendar year.

If you want to give more than the QCD limit, you still can, but amounts above the limit would generally be treated like normal taxable IRA distributions.

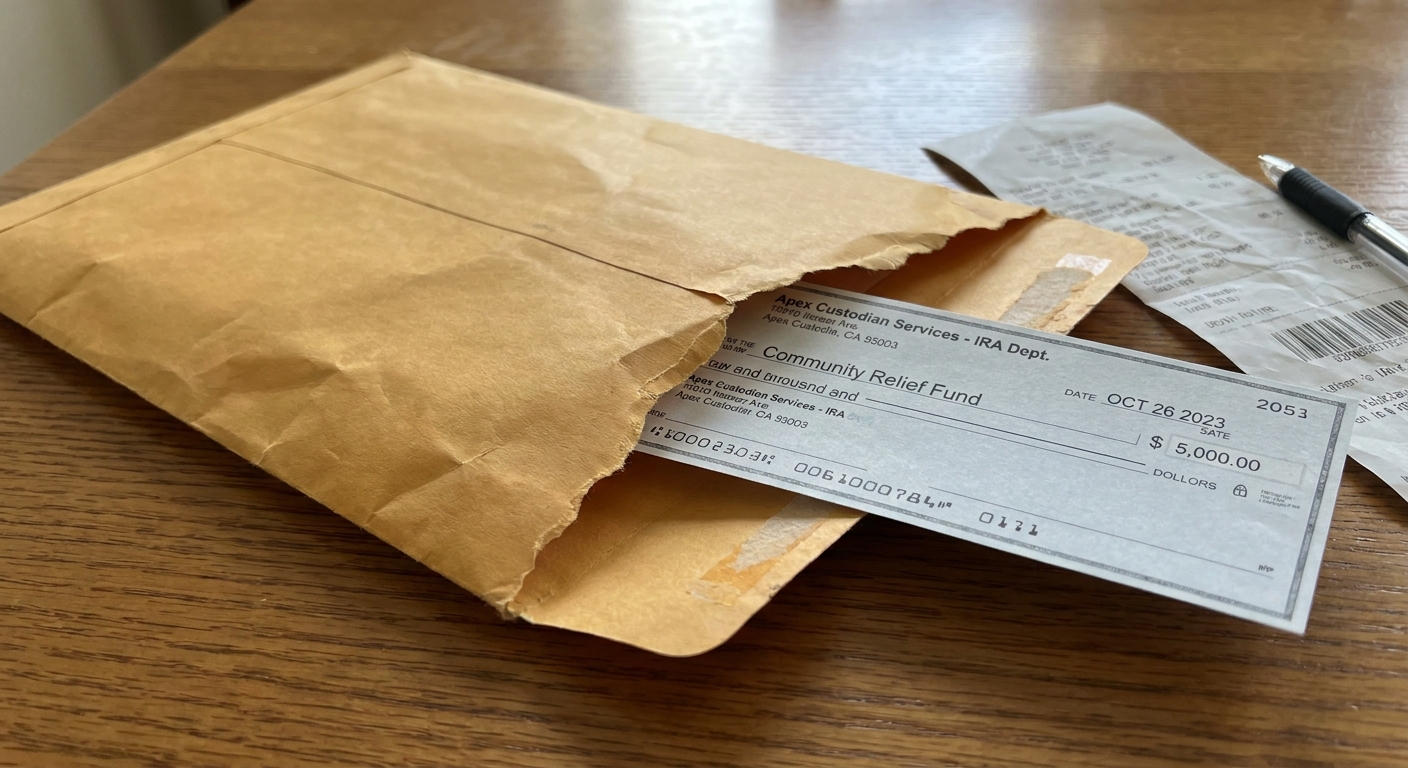

The direct-to-charity rule (do not break this)

A QCD must go directly from your IRA custodian to the charity. If the money touches your hands first, you have likely just created a regular taxable distribution.

What “direct” usually looks like in real life

- Your IRA custodian sends a check payable to the charity and mails it to you to deliver, or mails it straight to the nonprofit.

- Some custodians can send funds electronically to the charity, depending on their systems.

What you want to avoid:

- Taking a distribution to your personal bank account and then writing your own check.

- Having the check made payable to you (even if you plan to endorse it to the charity).

QCDs and RMDs in 2026

If you are in an RMD year, a properly executed QCD can count toward satisfying your required minimum distribution for that year.

Here is the key detail: the IRS generally treats distributions as coming out of your IRA in the order they occur. So if you want your QCD to reduce your RMD burden, it is smart to do the QCD before taking other IRA withdrawals for the year.

Simple example

Let’s say your 2026 RMD is $25,000. You plan to donate $10,000 to charity anyway.

- If you do a $10,000 QCD, you may only need to withdraw $15,000 more to meet your RMD.

- If instead you withdraw the full $25,000 into your checking account first and later donate $10,000 from cash, you might end up with higher taxable income, especially if you do not itemize.

One more timing pitfall: QCDs must clear your IRA by December 31 to count for that tax year. Waiting until late December can be risky if your custodian is backed up.

What qualifies (and what does not)

Typically qualifies

- Donations to eligible 501(c)(3) public charities.

- Churches, many local nonprofits, food banks, animal shelters, and similar operating charities (as long as they are eligible to receive tax-deductible contributions).

Does not qualify (common deal-breakers)

- Donor-advised funds (DAFs)

- Private foundations in many cases

- Supporting organizations (often ineligible for QCD purposes)

- Anything that provides you a benefit such as gala tickets, auction items, or membership perks. QCDs are meant to be a pure charitable gift.

- Pledges can be tricky. Many taxpayers want a QCD to satisfy a pledge. Whether it is acceptable depends on specifics, and charities handle pledges differently. If you are trying to satisfy a pledge with a QCD, check with the charity and a tax pro before you send it.

My rule of thumb: if your donation involves a “thank you gift,” a seat at a table, or anything that feels like a purchase, do not run it through a QCD.

New option: one-time split-interest QCD

SECURE 2.0 added a twist that is worth knowing for 2026 planning: a one-time QCD can be used to fund certain split-interest charitable vehicles.

In plain terms, this can allow a one-time QCD to go into a charitable gift annuity (CGA), a charitable remainder unitrust (CRUT), or a charitable remainder annuity trust (CRAT), assuming all the technical requirements are met.

The cap started at $50,000 and is indexed for inflation, so the allowable amount may be higher by 2026. This is a popular idea for retirees who want to support a charity and also create an income stream, but it is detail-heavy. If you are considering it, it is worth coordinating the charity, your custodian, and your tax pro before you move a dollar.

QCD vs donor-advised fund

People often confuse QCDs and donor-advised funds because both are popular charitable strategies.

- QCD: Great for retirees who want to give now from an IRA and keep that amount out of taxable income. It is especially powerful in RMD years.

- Donor-advised fund: Great for people who want to “bunch” deductions in a high-income year, donate appreciated assets, then grant money to charities over time. But QCDs cannot be contributed to a DAF.

If your goal is to reduce IRA taxable withdrawals and you are already 70½ or older, QCD is usually the first place I look.

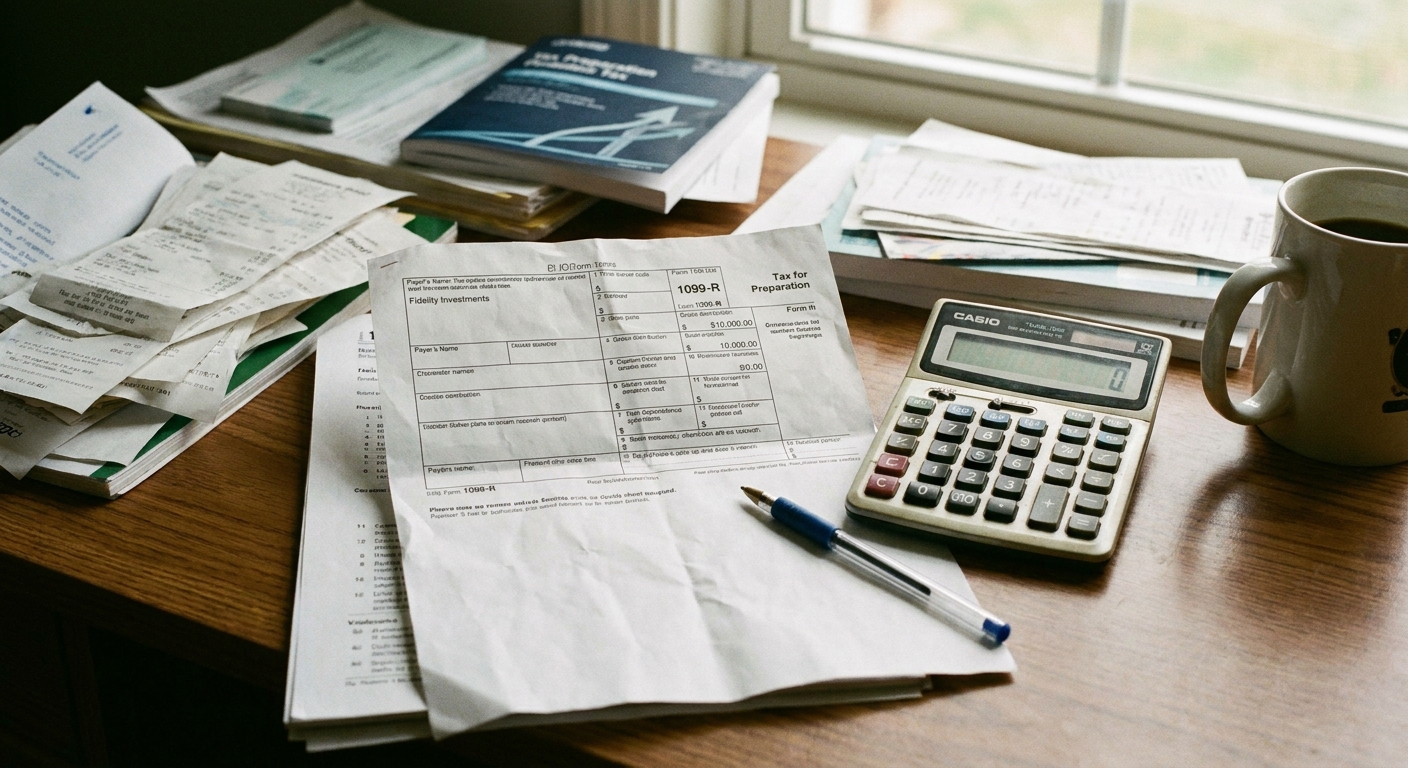

1099-R mistakes that cost people money

This is where a lot of perfectly good QCDs get messy. Your IRA custodian will report the distribution on Form 1099-R, but they usually do not label it as a QCD.

That means it is on you (or your tax preparer) to report it correctly on your tax return.

The most common QCD reporting issues

- Assuming the 1099-R will say “QCD.” Most of the time it will not. It may look like a normal distribution.

- Reporting the full distribution as taxable. If you miss the QCD entry, you can accidentally pay tax on money that should have been excluded.

- Taking a charitable deduction anyway. A QCD is not both an income exclusion and an itemized deduction. No double-dipping.

- Not keeping charity documentation. You still need the charity’s written acknowledgment for contributions when required, and you should keep proof the funds went directly to the organization.

- Withholding taxes from the distribution. QCDs should generally be a clean transfer to charity. If you withhold taxes, that withheld portion is not going to the charity and can complicate how much is treated as a QCD.

How it often shows up on Form 1040

The mechanics vary by tax software, but a common approach is:

- Report the full IRA distribution on Form 1040, Line 4a.

- Report the taxable amount on Line 4b as 0 (or as reduced by the QCD amount if only part of the distribution was a QCD).

- Write “QCD” next to Line 4b.

Practical tip: When you do a QCD, save a small folder with (1) the IRA distribution confirmation, (2) the check copy or transaction proof, and (3) the charity acknowledgment letter. If you ever need to explain it, you will be glad you did.

Step-by-step: how to do a QCD cleanly

- Confirm you are eligible (70½ or older on the distribution date).

- Confirm the charity is eligible for QCD purposes (ask the nonprofit, or verify their status).

- Contact your IRA custodian and request a QCD check payable to the charity.

- Decide on timing so it clears by December 31, and ideally before you take other IRA withdrawals if you are using it toward your RMD.

- Get a written acknowledgment from the charity and keep it with your records.

- Tell your tax preparer the distribution was a QCD and provide the amount and charity details.

Quick FAQ for 2026 QCD planning

Can I do a QCD from my Roth IRA?

Roth IRA distributions are often already tax-free, so a QCD from a Roth typically does not create the same benefit. QCDs are mainly used with pre-tax IRA money. If you are considering it anyway, confirm the rules with your custodian and tax pro.

Can I do a QCD and still take the standard deduction?

Yes. That is one of the best parts. A QCD can reduce taxable income even if you do not itemize.

Does a QCD help with IRMAA?

Potentially, yes. Because QCD amounts are generally excluded from income, they can reduce modified AGI, which is what Medicare uses to determine IRMAA surcharges. It is not guaranteed for every situation, but it is one reason QCDs are so popular.

What if I already took my full RMD for the year?

You can still give to charity, but a QCD made after you already withdrew your RMD may not provide the same planning benefit. It can still exclude the QCD amount from income if done correctly, but you cannot “undo” an RMD you already took. Timing matters.

My bottom line

If you are 70½ or older and you donate every year, QCDs are worth a serious look in 2026. They are one of those rare moves that can feel like a win-win: you support causes you care about, and you may keep your tax picture calmer at the same time.

If you want, tell me your age, whether you are taking RMDs yet, and roughly how much you give annually. I can help you think through a clean QCD game plan and the biggest pitfalls to avoid.