If you get paid every two weeks, you have probably had this exact thought: “I make decent money, so why does my account feel tight right before rent?”

You are not bad at budgeting. You are just dealing with a scheduling mismatch. Most bills show up monthly, but your paychecks show up every 14 days. That creates a weird rhythm where some months feel flush and some feel like a scramble.

In this guide, I will show you how to align a biweekly paycheck with monthly bills using a simple calendar method. No apps required. Just a plan you can run on paper, in Notes, or in a basic spreadsheet.

Why biweekly pay feels tight twice a year

Biweekly pay means you get 26 paychecks per year. Monthly bills happen 12 times per year.

If you do the math, 26 paychecks is the same as getting paid “twice a month” most of the time, plus two extra paychecks somewhere during the year.

The squeeze happens when you budget like you only get two checks

Many of us accidentally build a monthly budget assuming two paychecks will land in every month. But two months each year, you will receive three paychecks, and the timing around bill due dates can make things feel chaotic.

- Some months have a long gap between a paycheck and a big bill like rent or a mortgage.

- If you pay bills “when they come in” rather than with a plan, the month can get front-loaded.

- If that third paycheck gets spent casually, the months that follow can feel painfully tight.

The goal is to make your money feel monthly even when your pay is biweekly.

Pick a system: two-paycheck plan or half-month plan

There are two simple ways to organize a biweekly budget. Both work. The best one is the one you will actually keep up with.

Option A: The two-paycheck plan (my favorite for beginners)

You assign certain bills and categories to Paycheck 1 and the rest to Paycheck 2. This works best when your bills are fairly predictable.

- Paycheck 1: rent or mortgage, core utilities, insurance, minimum debt payments

- Paycheck 2: groceries, gas, sinking funds, subscriptions, extra debt payoff, fun money

This creates a repeatable rhythm: every check has a job.

Option B: The half-month plan (best if your bills cluster)

You treat the month as two halves:

- Days 1 to 15

- Days 16 to end of month

Then you assign bills based on due dates. This method is great if most of your bills are due at the beginning of the month and you want to stop feeling behind by day five.

If you are not sure, start with the two-paycheck plan. It is easier to maintain when your paydays shift around the calendar.

The simple calendar method (no app required)

All you need is a calendar (paper or digital) and a list of your bills.

Step 1: Mark your paydays for the next 2 to 3 months

Because biweekly pay moves through the calendar, you want to see the pattern, not guess it.

- Circle each payday.

- Write your expected take-home pay amount next to it if it varies.

Step 2: Write down every monthly bill with the due date

Include the boring stuff and the sneaky stuff:

- Housing (rent or mortgage)

- Electric, gas, water, trash

- Internet and phone

- Car payment, insurance

- Minimum debt payments

- Subscriptions and memberships

- Childcare, tuition, therapy, medications

Then place each bill on the calendar on its due date.

Step 3: Assign each bill to the paycheck that happens right before it

Look at a bill due date, then look backward to the most recent payday. That bill belongs to that paycheck.

If a bill is due within 1 to 3 days of payday, you can assign it either way. Pick the option that reduces stress.

Step 4: Create two lists for each paycheck

On a separate sheet (or note), make a simple template you will reuse:

- Paycheck Date:

- Bills to pay before next paycheck:

- Spending until next paycheck (groceries, gas):

- Sinking funds:

- Extra goals (debt payoff, saving):

This is the whole system. You are just pairing each bill to a specific paycheck so nothing is floating in your head.

How to handle the “extra” paycheck months

Those two months with three paychecks are not a bonus to blow by default. They are a chance to get ahead and make the rest of the year easier.

Here is the rule I wish someone had drilled into me when I was climbing out of debt:

Do not let your lifestyle automatically expand to match your third paycheck. Give it an assignment before it hits.

Where to stash the extra check money (three good options)

Pick one based on your current stage.

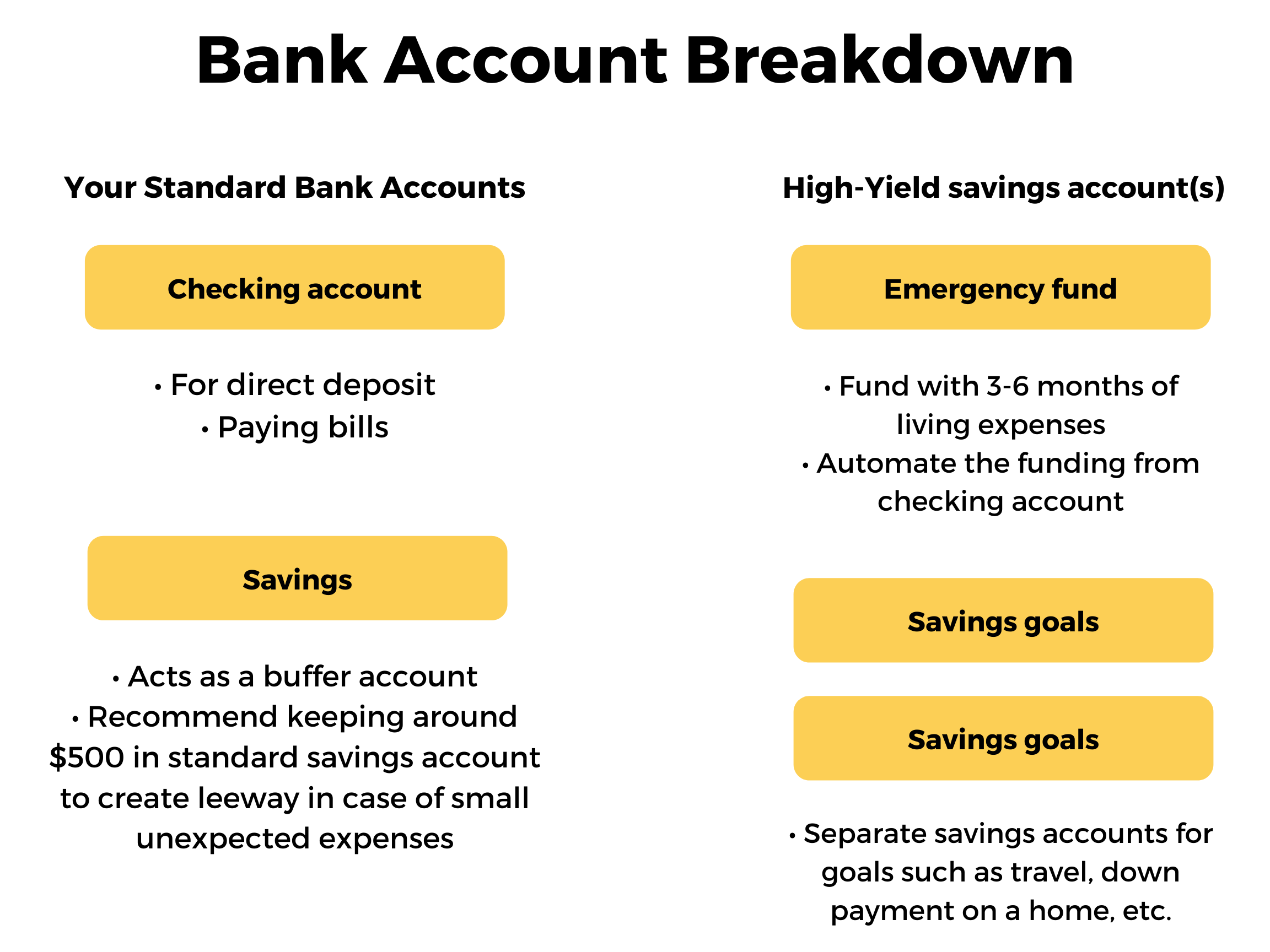

- Option 1: A separate “bill buffer” savings account. This is the cleanest choice. Park the extra paycheck here and pull from it when a month feels tight. A high-yield savings account works great because the money is safe and a little harder to impulse-spend.

- Option 2: A dedicated checking sub-account if your bank offers it. Label it “Monthly Bills” or “Buffer.” This is helpful if you prefer everything inside your bank.

- Option 3: Pay down high-interest debt. If you have credit cards at 20% to 30% APR, using an extra paycheck here can save you serious money and reduce future monthly pressure.

If you want a simple order of operations: build a small buffer first, then attack high-interest debt, then build a larger buffer and sinking funds.

The two-paycheck template you can copy

Use this as a starting point and adjust it to your bills.

Paycheck 1 (the “keep the lights on” check)

- Rent or mortgage

- Electric and gas

- Water and trash

- Insurance (auto, renters, health premiums if applicable)

- Minimum debt payments

- Set aside enough for groceries and gas until the next paycheck (about 2 weeks).

Paycheck 2 (the “life happens” check)

- Phone and internet

- Subscriptions (or cancel a few, your call)

- Set aside enough for groceries and gas until the next paycheck (about 2 weeks).

- Sinking funds (car repair, gifts, vet, annual fees)

- Extra debt payoff or saving

- Fun money, with a cap

Two notes from someone who used to overdraft like it was a hobby:

- Fund groceries on both checks. Your paycheck has to cover the entire time until the next one. If you only fund one week, week two gets ugly fast.

- Build sinking funds on purpose. Most “surprise” expenses are not surprises. They are just irregular.

Make monthly bills feel monthly with a buffer

If you want your budget to feel calm, the real unlock is a buffer.

A buffer is simply money you keep so you are not relying on perfect timing. Even a small one helps.

Start with a $500 to $1,000 mini buffer

This prevents small timing issues from turning into overdrafts or credit card swipes.

Work toward a one-month buffer (eventually)

This is the dream setup: you pay this month’s bills using last month’s income. When you reach this point, payday stops being a crisis and starts being a routine deposit.

You can build a one-month buffer using:

- one or two “extra” paychecks

- tax refunds (if you are not carrying high-interest debt)

- small monthly transfers like $50 to $200

Common pitfalls (and quick fixes)

Pitfall: Paying bills early just because money is there

Fix: Pay according to your plan. If you pay everything early, you can accidentally drain the cash you need for groceries and gas during the same pay period.

Pitfall: Forgetting non-monthly expenses

Fix: Add sinking funds. Examples: car registration, holiday gifts, annual subscriptions, back-to-school, vet visits.

Pitfall: Treating the third paycheck as spending money

Fix: Decide in advance: buffer, debt, or sinking funds. If you want to enjoy some of it, great. Just set a percentage, like 10% fun and 90% goals, so it still moves your life forward.

Pitfall: Your due dates are working against you

Fix: Call your providers and ask to move due dates. Many lenders and utilities will let you shift a due date once. Getting most bills to land after your first paycheck can reduce stress immediately.

A quick example: how this looks in real life

Let’s say you get paid every other Friday and rent is due on the 1st.

- If you have a paycheck around the 20th to 25th, assign rent to that paycheck and move the rent money into your bills account immediately.

- Your next paycheck (around the 3rd to 10th) covers mid-month bills and spending until the next paycheck.

Notice what we did: we stopped letting the calendar decide whether rent feels stressful. We assigned it to a specific paycheck every time.

Bottom line

Biweekly pay is not the problem. The mismatch between paycheck timing and monthly bills is the problem, and it is fixable.

Use the calendar method to assign each bill to a specific paycheck, then stash the “extra” paycheck money in a bill buffer account (or pay down high-interest debt). After a month or two, your budget starts to feel predictable, and predictable is where financial peace lives.

If you want to take one small step today: pull up the next two months on a calendar, circle paydays, and assign rent to a paycheck. That one move alone can change your whole month.