Seeing “collections” next to a medical bill can make your stomach drop. I have been there with money stress, and I know the first impulse is to either panic-pay or ignore it and hope it goes away.

Instead, slow down and do this in order: verify the amount, make the collector prove they have the right to collect , dispute errors, and choose the least-damaging way to resolve it. Medical billing is messy, insurance processing takes time, and mistakes are common. Your job is to keep this from turning into a bigger financial and credit problem than it needs to be.

Note: This article is U.S.-specific and focuses on common federal protections and major credit bureau policies. State laws and reporting policies can vary and can change.

First: Confirm what you are being billed for

Before you talk payment plans, settlements, or credit reports, you need to confirm whether the balance is real and whether it is already supposed to have been covered by insurance or financial assistance.

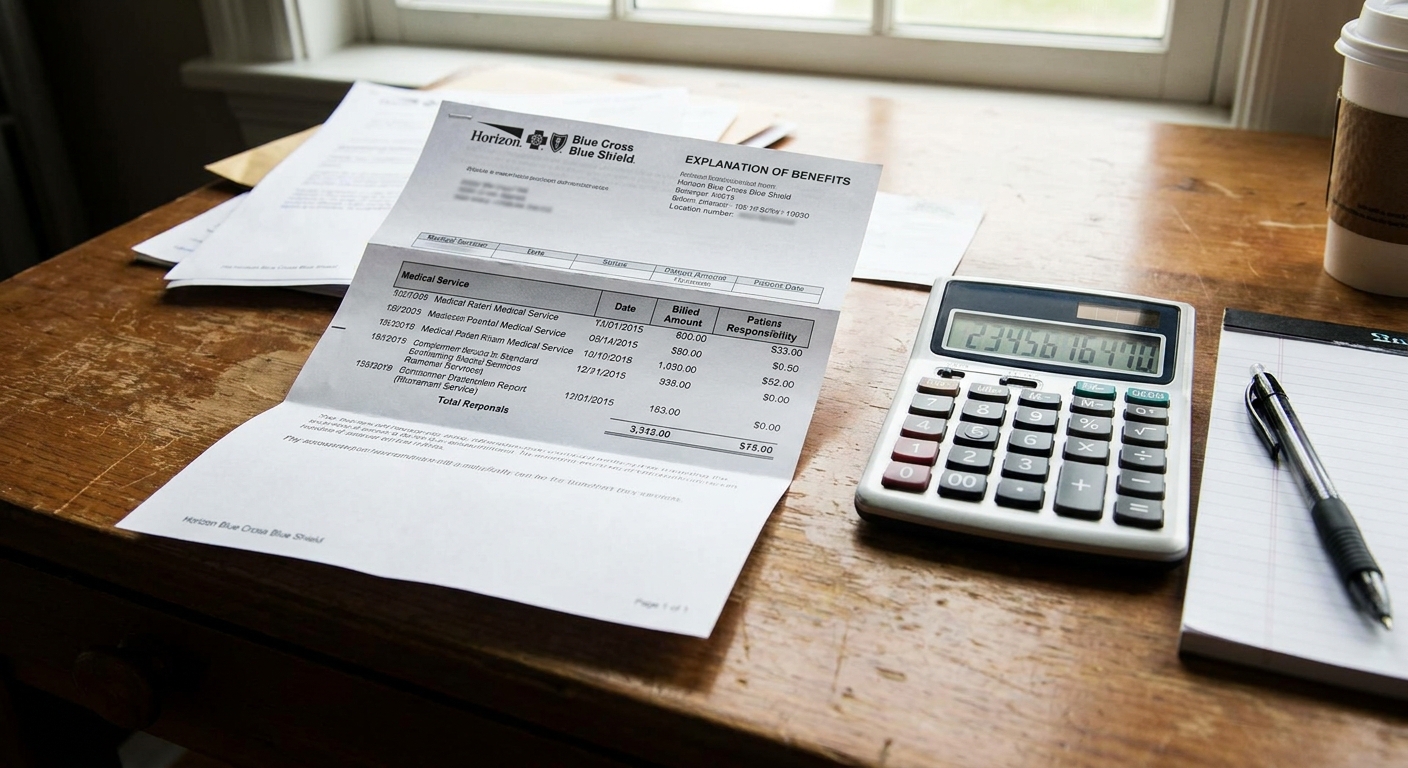

EOB vs provider bill: not the same

EOB stands for Explanation of Benefits. It comes from your insurer and explains how the claim was processed. It is not a bill. A provider bill comes from the hospital, clinic, lab, or doctor’s office asking you to pay.

- EOB: what was billed, what was allowed, what insurance paid, and what the plan says you may owe (copay, deductible, coinsurance, non-covered).

- Provider bill: what the provider says you owe right now and where to pay it.

- Collections notice: a collector saying you owe a debt they are attempting to collect, often after the provider sent it out.

Common reasons the numbers do not match:

- The claim is still processing or was reprocessed.

- The provider billed the wrong insurance, wrong member ID, or wrong date of birth.

- The provider is out of network, or the claim was coded incorrectly.

- You were billed for something that should have been included (duplicate charges, cancelled procedure, wrong patient).

- The provider never applied your payment, HSA payment, or charity care approval .

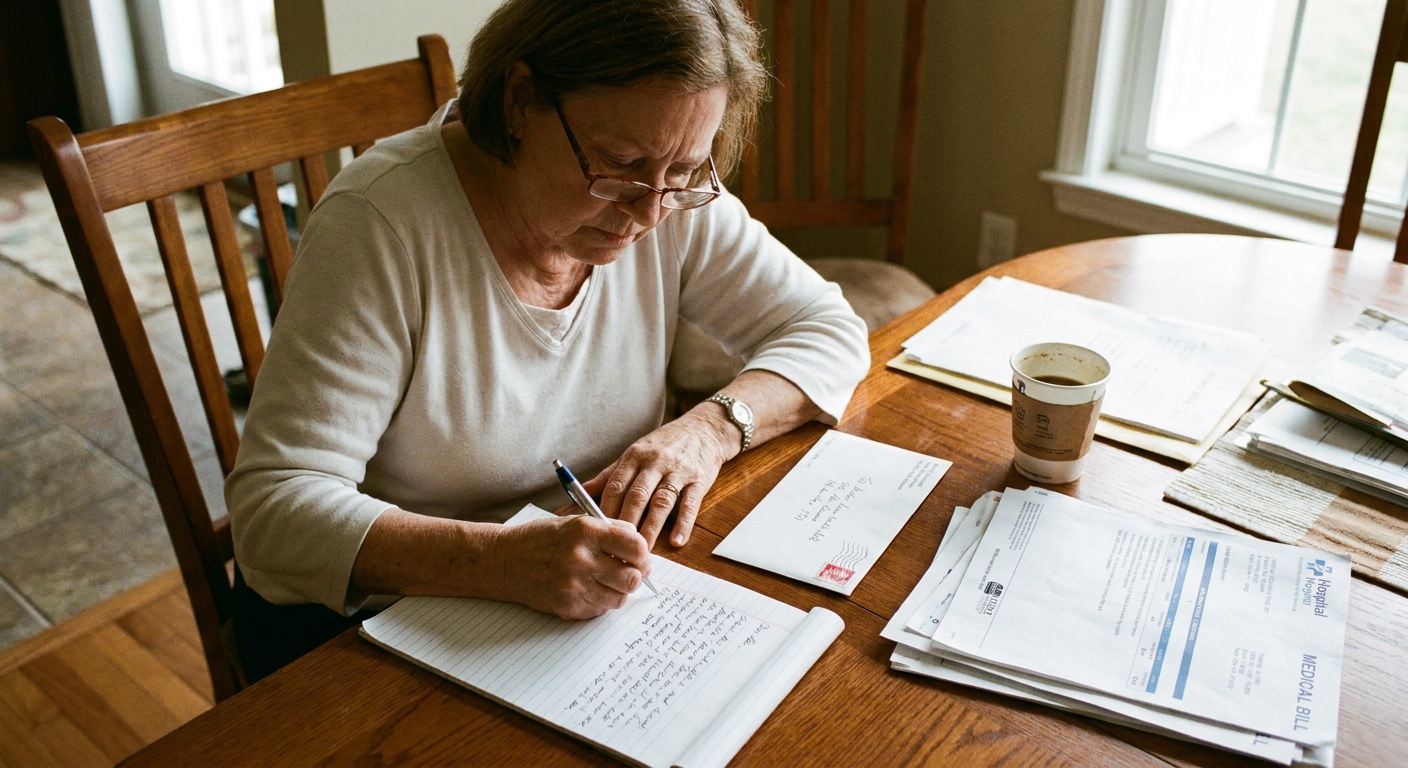

Your 10-minute paperwork checklist

- The collections letter (front and back), including the amount, account number, and the name of the current collector.

- The most recent provider statement(s) for that date of service.

- Your EOB(s) for the same date of service (log in to your insurance portal if needed).

- If you had multiple providers at one visit (ER doctor, hospital facility, lab, radiology), list them separately. One ER trip can produce 3 to 6 different bills.

Know your rights with collectors (FDCPA basics)

Most third-party debt collectors must follow the Fair Debt Collection Practices Act (FDCPA). That law does not erase legitimate debt, but it does give you rights around information, timing, and harassment.

Debt validation: make them prove it

After a collector first contacts you, they typically must send a written validation notice within five days. You generally have 30 days from receiving that notice to request validation in writing. If you request validation within that 30-day window, the collector generally must pause collection efforts until they provide verification.

Goal: do not pay a collector until you have enough information to confirm the debt is yours, the amount is accurate, and they have the right to collect.

What to ask for in your validation request:

- The name and address of the original creditor (the medical provider).

- The date(s) of service tied to the balance.

- An itemized statement or breakdown showing how the amount was calculated.

- Proof they are authorized to collect on this debt (or that they own it, if it was sold).

- Information about any interest, fees, or adjustments added after the provider billed it.

Important: keep everything in writing, and keep copies. If you call, take notes with dates, times, and the name of the person you spoke with.

If the provider is collecting directly

If the hospital or doctor’s office is collecting with its own billing department, FDCPA may not apply the same way it does to third-party collectors. Even then, you can still request itemization and proof, and you should still insist on accurate billing.

Step-by-step: When medical debt hits collections

Step 1: Be careful on the phone

You can say, “I am requesting details in writing,” and end the call.

Also, be cautious about making any payment or agreeing to anything before you have details. In some states, partial payments or certain acknowledgments can affect the statute of limitations . The safest move is to validate first, then decide.

Step 2: Request itemization from the provider

Call the provider’s billing office and ask for an itemized bill and the status of the insurance claim. Ask:

- Was insurance billed? Which insurance?

- Was the claim denied, pended, or paid?

- Is there an internal hold they can place while you resolve insurance?

- Can they recall it from collections if it is incorrect or if you set up an arrangement?

Step 3: Send a validation request to the collector

Send a written request for validation (certified mail can be worth it for the paper trail). If you send it within the FDCPA 30-day window, the collector generally must pause collection until they provide verification.

Step 4: Dispute with the right party

Medical billing problems usually have one of three “homes,” and you want to dispute with the one that can actually fix it:

- Insurance dispute or appeal: if the EOB shows a denial, out-of-network issue, or medical-necessity decision you believe is wrong.

- Provider billing dispute: if the itemized bill is wrong, duplicate, coded incorrectly, or missing payments or adjustments.

- Collector dispute: if the collector has the wrong amount, wrong person, wrong provider, or cannot validate.

Step 5: If it is correct, pick a resolution strategy

Once you are confident the bill is legitimate, you have options that can reduce cost and protect your credit. The best option depends on your cash flow, the balance size, and whether the account is already appearing on your credit reports.

Who to pay and how to document it

Before you pay anyone, confirm who currently controls the account.

- If the provider can take payment and agrees (in writing) to recall the account from collections, that can simplify things.

- If the debt was sold, you may need to resolve it with the collector or the debt buyer.

Either way:

- Get the terms in writing before paying (settlement or payment plan).

- Pay in a trackable way and keep receipts.

- Ask for a zero-balance letter or “paid in full” confirmation after the final payment.

Negotiation strategies that work

Medical debt is one of the few areas where negotiation is common and not weird. The system is built around adjustments, contracted rates, and financial assistance.

Ask about financial assistance first

Before offering a settlement number, ask the provider (or sometimes the collector, depending on who controls the account) about:

- Charity care or financial assistance programs.

- Prompt-pay discounts if you can pay in full.

- Income-based discounts even if you have insurance.

If you qualify, you may get the balance reduced significantly, sometimes even retroactively depending on the provider’s policy.

Payment plan: negotiate the terms

If you need a plan, focus on:

- Low or zero interest and minimal fees (many providers offer this, but it is not guaranteed, so ask directly).

- A payment you can keep even during a rough month.

- A written agreement that the plan satisfies the debt as long as you make payments.

A tiny payment you can reliably make beats an aggressive plan you will break.

Lump-sum settlement: get it in writing

If you can offer a one-time payment, ask whether they will accept a reduced amount as settlement in full . Key rules:

- Get the settlement terms in writing before you pay.

- Confirm the settlement amount and the date it must be received.

- Pay in a trackable way (online portal receipt, money order, or another method you can document).

Try a goodwill recall if insurance caused the mess

If the bill went to collections because insurance was delayed or information was incorrect, ask the provider to pull the account back from collections once the claim is corrected, then request a new statement reflecting the proper insurance adjustment.

No Surprises Act: when it matters

The No Surprises Act is designed to protect patients from certain unexpected out-of-network bills, especially in emergencies and some situations at in-network facilities.

It generally applies to people with most private health insurance. It does not apply to Medicare or Medicaid in the same way, and federal protection generally does not cover ground ambulance bills.

Situations that may qualify

- Emergency care where you did not choose an out-of-network provider.

- Out-of-network providers at an in-network hospital or facility in certain circumstances.

- Air ambulance services are covered under the federal protections in many situations.

What to do if you suspect a surprise bill

- Ask the provider for the diagnosis and procedure codes and whether the claim was processed as out-of-network.

- Ask your insurer whether the claim should be protected under the No Surprises Act.

- Request any required notices or consent forms you would have had to sign to waive protections.

- Escalate through your insurer’s appeals process if needed.

If you were improperly balance-billed, paying a collector first can make the cleanup harder. Validate and dispute before you pay.

How medical collections affect your credit

Medical collections are treated differently than many other collection accounts, and the rules have changed in recent years. Always verify what is currently reporting on your credit file.

What the major bureaus have done (as policies)

- Waiting period: Unpaid medical collections typically are not reported to the credit bureaus until about 365 days after the account becomes delinquent, based on major bureau policy changes.

- Paid collections: The three major credit bureaus removed paid medical collection debt from consumer credit reports under prior policy updates. If you pay or settle, it is worth checking that your reports update correctly.

- $500 threshold: Medical collections under $500 have been excluded from reporting under major bureau policies. This is policy-based and could change.

What “aging” means: once a collection is reported, its impact generally fades over time, but the account can remain on your reports for years if it is not resolved. The credit damage is usually worst early on.

Protect your credit while you work the process

- Do not ignore notices. The fastest path to credit damage is silence.

- Get everything in writing and keep a simple folder (digital or paper).

- Check your credit reports from all three bureaus to see whether the account is reporting and whether the amounts match.

- Dispute inaccurate reporting with the credit bureaus if the information is wrong or cannot be validated.

Privacy note: Medical collections on credit reports generally do not include diagnosis details, but the financial account can still hurt your credit if it is reported.

Extra-important: Even if you are focused on credit, do not lose sight of the bigger risk. A collector may also pursue legal action depending on your state’s rules and the balance size.

If you get sued or receive court papers

If you receive a summons, complaint, or any court notice, do not set it aside.

- Respond by the deadline. Missing it can lead to a default judgment.

- Get help fast. Consider legal aid in your area or a consumer law attorney, especially if the amount is large or you believe the debt is not valid.

- Bring your paper trail. Your EOBs, itemized bill, validation request, and any letters matter.

What to say and what to ask

To the collector: request validation

“I am requesting validation of this debt. Please provide the original creditor, the date of service, an itemized breakdown of the amount, and documentation showing you are authorized to collect. I prefer all communication in writing.”

To the provider: request itemization and insurance status

“Can you send me an itemized bill for this date of service and confirm what insurance was billed? Also, can you confirm whether any payments, adjustments, or financial assistance were applied and whether the account can be placed on hold while we resolve this?”

To negotiate a settlement (once verified)

“I can pay $___ as a one-time payment if you will accept it as settlement in full. If you agree, please send the terms in writing before I submit payment.”

Mistakes that cost people money

- Paying the first notice without checking the EOB. You can accidentally pay what insurance should have covered.

- Assuming one ER visit equals one bill. Facility, physician, lab, and imaging bills often come separately.

- Making a good faith payment before you have details. In some situations, it can complicate disputes, and in some states it can affect the statute of limitations.

- Not getting agreements in writing. If it is not written, it is not real.

- Letting shame run the show. Medical debt is common. You are not a bad person for having it.

A simple plan to prevent this next time

This is not the part where I tell you to “just budget harder.” But once you are putting out a collections fire, it helps to build a small buffer so the next surprise does not go straight to your credit.

Two realistic moves

- Start a medical mini-fund: even $25 per paycheck in a separate savings bucket can cover copays, prescriptions, or a first payment to keep an account from escalating.

- Use a one-page billing tracker: date of service, provider, amount billed, EOB status, what you paid, and who you spoke with. Boring, yes. Powerful, also yes.

If you take nothing else from this: do not pay medical debt in collections until you have matched the bill to your EOB and gotten validation in writing.

Where to get help

- Provider financial assistance office: Ask for the charity care or financial assistance application and the policy.

- Your insurer: Use the appeals process for denials and out-of-network disputes, and ask about No Surprises Act protections when relevant.

- CFPB: You can submit a complaint for debt collector issues or inaccurate collection information.

- Your state insurance department: Helpful for some coverage and claims disputes.

- Credit reports: Pull your reports at AnnualCreditReport.com and verify what is actually reporting.

Quick FAQ

Should I pay a medical collection immediately to protect my credit?

Not immediately. First verify the debt and amount. If it is legitimate, paying or settling can help, especially since paid medical collections have been removed from reports under major bureau policies. But validation and accuracy come first.

Can I dispute medical debt on my credit report?

Yes. If the reporting is inaccurate, the amount is wrong, the account is not yours, or it cannot be validated, you can dispute with the credit bureaus. Keep documentation.

What if I already paid but it is still on my report?

Keep your receipt and settlement letter, then check whether the account updated properly. If it is not updating, dispute the reporting with documentation.

Your next three moves

- Pull the EOB and provider bill for the same date of service and compare line by line.

- Request itemization from the provider and validation from the collector in writing (especially within the 30-day FDCPA window).

- If the bill is correct, negotiate: financial assistance first, then a manageable plan or a written settlement.

Want a simple way to stay organized? Download or make a one-page tracker and keep every letter, EOB, bill, and phone note in one folder until the balance is resolved and your reports reflect it.