If you have ever looked at your paycheck stub and thought, “Where did my money go?”, you are not alone. I used to stare at mine when I was buried in debt, trying to figure out why my take-home pay never matched what I mentally calculated in my head.

The good news: once you know the handful of sections every pay stub uses, it gets simple fast. In this guide, we will walk line-by-line through a typical stub, decode the most common deductions and tax withholdings, and show you exactly what to check when something looks off.

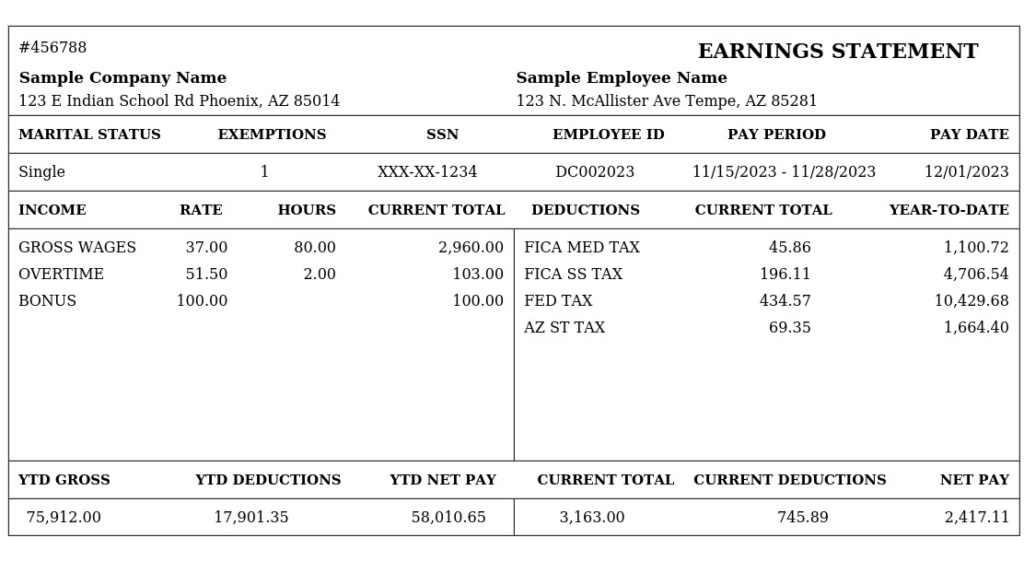

Start here: the 6 parts almost every pay stub has

Most payroll providers format stubs differently, but the core pieces are usually the same:

- Employee and pay period info (who, when, how often you are paid)

- Earnings (gross pay details like hourly rate, hours, salary)

- Pre-tax deductions (benefits that can reduce taxable income)

- Taxes withheld (federal, state, and FICA)

- Post-tax deductions (items taken out after taxes)

- Net pay (your actual take-home amount)

Quick distinction that helps: tax withholdings are amounts sent to tax agencies. Deductions are other items taken out of your pay (like benefits or retirement contributions).

Many stubs also show current amounts (this paycheck) and YTD amounts (year-to-date totals).

Employee info and pay period

At the top, you will usually see your name, partial Social Security number or employee ID, and the pay period dates (for example, “03/01 to 03/15”) plus the pay date.

What to verify

- Pay period dates: Your hours, overtime, and PTO should match this window.

- Pay frequency: Weekly, biweekly, semimonthly, or monthly changes how deductions are spread out.

- Direct deposit account: Some stubs show the last 4 digits. Make sure it is your account.

If you ever feel like a check is “short,” the pay period dates are the first place I look. A mismatch here can explain a lot.

Earnings (gross pay)

Gross pay is your pay before anything is withheld. Your stub typically breaks gross pay into line items such as:

- Regular pay: Hourly rate times hours, or your salary amount for the period

- Overtime: Commonly 1.5x your regular rate for nonexempt employees under federal law, with variations by employer policy and state rules (and in some limited cases, double time)

- Bonus or commission

- PTO, holiday, or sick pay

- Retro pay: Corrections for prior periods

Common columns in earnings

- Rate: Your hourly wage or salary rate

- Hours: Regular and overtime hours worked

- Current: Amount earned this paycheck

- YTD: Total earned since January 1

Quick reality check: If you are hourly, multiply your rate by your hours. If it does not match your “Regular” line, you may have shift differentials, unpaid breaks, bonuses paid separately, or timing differences that payroll can clarify.

Bonus note (why bonuses feel “over-taxed”)

Bonuses and commissions are often treated as supplemental wages, and employers may withhold federal taxes using a different method than your regular paycheck. The result: the withholding on a bonus can look surprisingly high, even though your final tax owed is settled when you file.

Pre-tax deductions

Pre-tax deductions come out of your gross pay before certain taxes are calculated. This is why two coworkers with the same salary can have different take-home pay.

Common pre-tax deductions include:

- Health insurance premiums (medical, dental, vision)

- HSA contributions (Health Savings Account)

- FSA contributions (Flexible Spending Account)

- Traditional 401(k) or 403(b) contributions

- Pre-tax commuter benefits (in some workplaces)

Important nuance: not all pre-tax is pre-everything

Some deductions reduce federal and state income tax but not FICA (Social Security and Medicare). For example:

- Traditional 401(k) usually reduces federal income tax, but you still pay Social Security and Medicare on those wages.

- Section 125 (cafeteria plan) health premiums are typically excluded from federal income tax and FICA by default. There are exceptions depending on plan design and the specific benefit, so it is normal to see different “taxable wages” numbers across different tax lines.

If that sounded confusing, here is the takeaway: it is normal for “taxable wages” to differ depending on the tax line.

Taxes withheld

Your tax withholdings are estimates sent to the government throughout the year. Think of withholding as “paying as you go” so you are not hit with one giant bill in the spring.

Federal income tax (FIT)

This is your employer withholding federal income tax based on your Form W-4 and your pay. It depends on your filing status and any adjustments you made on the W-4.

Why it changes: bonuses, overtime, a W-4 update, or benefit changes can all move this line up or down.

State and local income tax

Not every state has income tax. If yours does, your stub may show state withholding and possibly local (city or county) tax depending on where you live and work.

Example: In Ohio, many workers see local tax for their city of employment or residence. Your stub may label it as “CITY,” “MUNI,” or the city name.

FICA: Social Security and Medicare

FICA is a payroll tax that funds Social Security and Medicare.

- Social Security tax is typically 6.2% of wages up to an annual wage limit.

- Medicare tax is typically 1.45% of wages. Additional Medicare tax can apply above certain income thresholds, and employers must start withholding it once your wages from that employer exceed $200,000 in a calendar year (even if your personal filing threshold is higher).

These rates are set by law, so if your wages match, the math is usually consistent. If Social Security tax suddenly stops later in the year, it can be because you hit the wage limit for that year.

Other taxes you might see

- SDI (State Disability Insurance) in certain states

- SUI (State Unemployment Insurance) is usually paid by employers, but some stubs display employer-paid taxes too

- Paid family leave payroll taxes in some states

Post-tax deductions

Post-tax deductions come out after taxes. These do not reduce your taxable income (though they may still be valuable).

Common post-tax deductions:

- Roth 401(k) contributions (taxed now, potential tax-free qualified withdrawals later)

- Garnishments (child support, creditor garnishments)

- Union dues (often post-tax)

- Life or disability insurance (depends on employer setup)

- Charitable giving payroll deductions

If you see a deduction you do not recognize, do not ignore it. Ask payroll or HR for the deduction name and the authorization on file.

Net pay

Net pay is the final number: gross pay minus all deductions and withholdings.

If you use direct deposit, your stub may also show how net pay is split across accounts (for example, $200 to savings, the rest to checking).

A simple sanity-check

- Start with gross pay.

- Subtract pre-tax deductions.

- Subtract taxes withheld.

- Subtract post-tax deductions.

- You should land on net pay.

A mini example

Let’s say your stub shows:

- Gross pay: $2,000

- Pre-tax deductions: $150 (health) + $100 (401(k)) = $250

- Taxes withheld: $220 total

- Post-tax deductions: $30 (Roth or union dues, for example)

Then your net pay should be: $2,000 minus $250 minus $220 minus $30 = $1,500.

YTD boxes

YTD means year to date. It shows totals from January 1 through this paycheck. These numbers are incredibly helpful for:

- Spotting errors that quietly repeat every pay period

- Estimating your annual income (especially if your pay varies)

- Checking retirement contributions and employer match progress

- Planning taxes if you owe or typically get a big refund

YTD numbers to watch

- YTD gross pay (total earnings)

- YTD taxable wages (often separate for federal, Social Security, Medicare)

- YTD federal and state withholding

- YTD 401(k) or HSA contributions

Pro tip from my spreadsheet-loving heart: once a quarter, jot your YTD gross pay and YTD federal withholding into a simple tracker. It makes tax season far less stressful.

Gross wages vs taxable wages

This is one of the most common “Wait, what?” moments on a pay stub.

- Gross wages: What you earned before any deductions.

- Taxable wages: What a specific tax is calculated on after certain pre-tax deductions.

- Subject wages: Another label some systems use for “wages subject to” a specific tax.

Because different deductions affect different taxes, you can see multiple taxable wage lines (federal, state, Social Security, Medicare) that do not match each other. That is usually normal.

Employer-paid items you might see

Some stubs include lines that are not coming out of your check but are still shown for transparency. Common examples:

- Employer 401(k) match

- Employer HSA contributions

- Employer-paid taxes (like certain unemployment taxes)

These can be great benefits, but they typically do not reduce your net pay.

Common pay stub codes

Payroll systems love short codes. Here are many of the ones you are most likely to see, and what they usually mean.

Earnings codes

- REG: Regular pay

- OT: Overtime

- PTO: Paid time off

- HOL: Holiday pay

- BON: Bonus

- COM: Commission

- RETRO: Retroactive pay adjustment

Tax codes

- FIT: Federal income tax withholding

- SIT: State income tax withholding

- SS or OASDI: Social Security tax

- MED: Medicare tax

- ADD MED: Additional Medicare tax (higher earners)

- LOC, MUNI, CITY: Local or municipal tax

Benefit and deduction codes

- 401K, 403B: Retirement plan contributions

- ROTH: Roth retirement contributions

- HSA: Health Savings Account contribution

- FSA: Flexible Spending Account contribution

- MED, DENT, VIS: Insurance premiums

- LTDI or STDI: Long-term or short-term disability insurance

Because employers label things differently, treat this list as a starting point. If you are unsure, ask for your company’s deduction code list.

When to adjust withholding

Your paycheck stub cannot tell you your final tax bill, but it can give you strong clues about whether you are on track.

Consider adjusting your W-4 if

- You owed a lot at tax time last year and it was not a one-off situation.

- You got a huge refund and would rather have more money in each paycheck.

- Your life changed: marriage, divorce, a new baby, a second job, a spouse started working, or you started freelancing.

- Your pay changed significantly due to a raise, commission change, or reduced hours.

What to do

- Update Form W-4 through your HR portal or payroll department. Most companies let you do this online.

- Use the IRS Tax Withholding Estimator to dial in your numbers. It is free and surprisingly helpful if you have your most recent stub in front of you.

- Recheck after 1 to 2 pay periods to confirm the change took effect.

My personal rule: I would rather make a small adjustment mid-year than panic in March when the tax bill shows up.

What to do if something looks wrong

Payroll mistakes happen. The faster you catch them, the easier they are to fix.

Run through this checklist

- Compare hours worked to your timecard or schedule.

- Check your pay rate if you recently got a raise or changed roles.

- Verify benefit deductions during open enrollment changes.

- Confirm tax withholdings if you changed your W-4.

- Look at YTD totals to see if the problem is new or has been repeating.

Who to contact

Start with your payroll contact or HR. If it is a timekeeping issue, your manager may need to approve a correction. Ask for the correction timeline and whether a supplemental check will be issued if you were underpaid.

Pay stub glossary

- Gross pay: Total earnings before any deductions or taxes.

- Net pay: Take-home pay after deductions and withholdings.

- Withholding: Money your employer sends to tax agencies on your behalf.

- Pre-tax deduction: Deduction taken out before certain taxes are calculated.

- Post-tax deduction: Deduction taken out after taxes are calculated.

- FICA: Payroll taxes for Social Security and Medicare.

- Taxable wages: The portion of your pay that a specific tax is calculated on.

- YTD: Year-to-date totals from January 1 through the current pay period.

- W-4: IRS form that guides your federal income tax withholding.

- W-2: Annual form summarizing wages and taxes for the year, often based on your final YTD totals.

The one habit that helps most

Pick one paycheck a month and do a quick review:

- Gross pay looks right

- Benefits look right

- Federal and state withholding look reasonable

- Net pay matches what hit your bank

That is it. You do not need to become a payroll expert. You just need to be the kind of person who notices when something changes. That small habit can save you hundreds, sometimes thousands, over a year.