Finding an error on your credit report can feel personal, like your finances are being judged by a messy file you did not even create. The good news is that disputing credit report errors is usually very doable if you stay organized, keep copies, and follow a clear process.

This guide walks you through pulling your reports, spotting mistakes, filing a dispute online or by mail, and following up with both the credit bureaus and the company that reported the information.

Before you dispute: know what you are looking at

Most credit scores and lending decisions are based on data from the three major credit bureaus:

- Equifax

- Experian

- TransUnion

Your credit reports can differ across bureaus because not every lender reports to all three. That is why you want to check each report separately.

What counts as an “error” worth disputing

Disputes work best for factual, verifiable mistakes. Examples include:

- Accounts that are not yours

- Incorrect balance, credit limit, or payment history

- Wrong dates (opened date, first delinquency date, payment dates)

- Duplicate accounts (same debt listed twice)

- Closed accounts reported as open, or vice versa

- Incorrect personal info that could indicate a mixed file (wrong name variation, wrong address, wrong employer)

- Incorrect status such as “late” when you have proof you paid on time

- Collections that should not be there, or are reported inaccurately

What disputes are not great for: “I do not like this account” or “this is unfair but accurate.” If the information is accurate, the bureaus typically will not remove it just because it hurts your score.

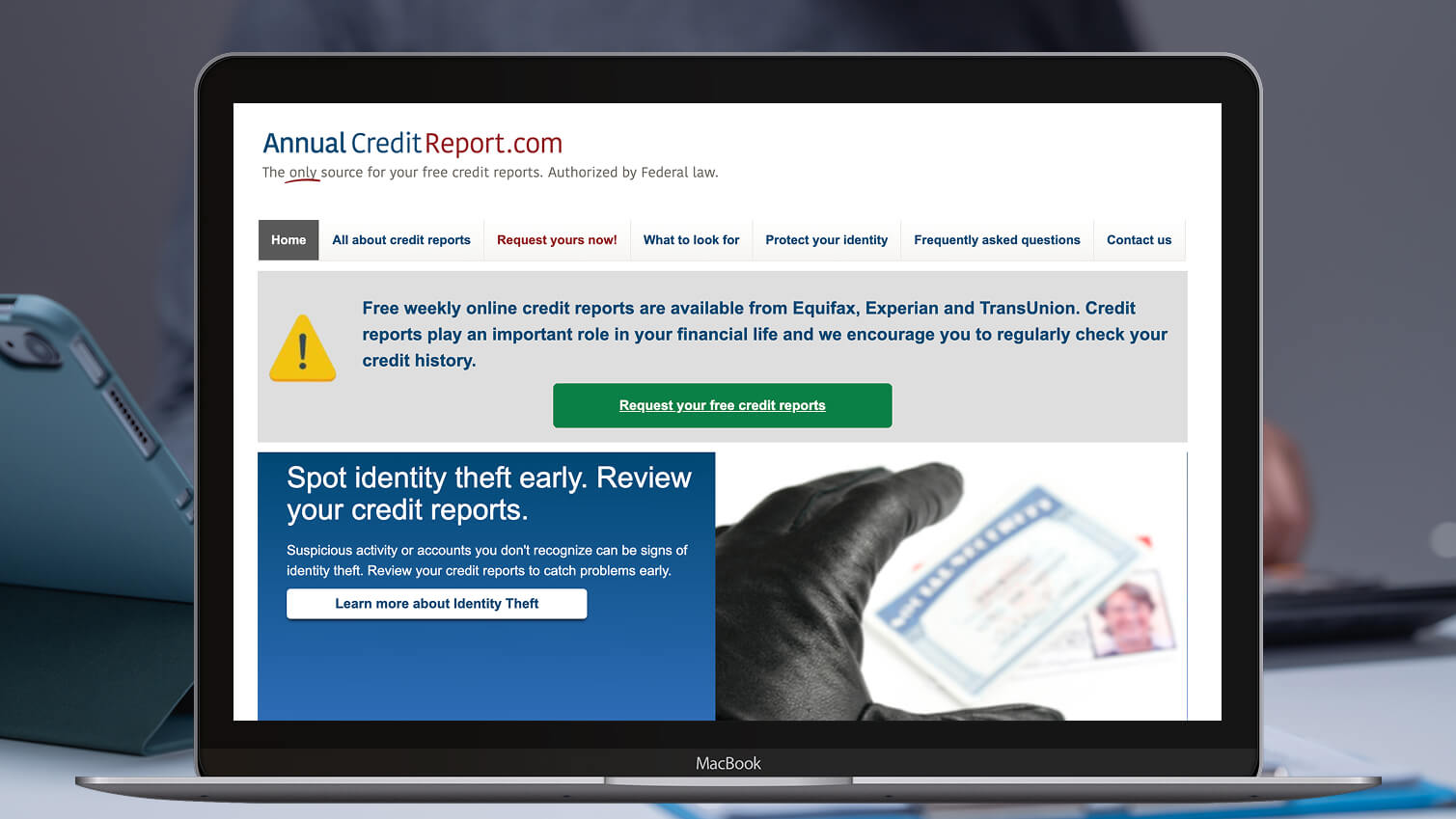

Step 1: Get all three of your credit reports

Start by pulling your reports from all three bureaus. The safest approach is to use the official source authorized by federal law: AnnualCreditReport.com.

When you download your reports:

- Save a PDF copy of each report

- Write down the date you pulled them

- Create a folder (digital or paper) for everything related to the dispute

If you are actively applying for a mortgage, car loan, or apartment, pull your reports sooner rather than later. Disputes can take time and can complicate underwriting if you open them mid-application.

Step 2: Scan for mistakes (use a simple system)

I like to scan reports in the same order every time, so I do not miss things. Here is a practical checklist-style flow.

Personal information

- Name spelling and variations

- Date of birth

- Current and past addresses

- Employers (not usually score-impacting, but odd entries can be a mixed-file clue)

Accounts (tradelines)

- Do you recognize every lender?

- Are open/closed statuses correct?

- Are balances and credit limits accurate?

- Any late payments that you can prove did not happen?

- Any duplicates?

Negative items: collections, charge-offs, public records

- Collections that are not yours or are reported with wrong amounts/dates

- Old negative items that might be too old to report (more on timelines below)

- Any judgments or bankruptcies that are clearly wrong (rare, but it happens)

Hard inquiries

Hard inquiries are typically from applications for credit. Dispute hard inquiries if:

- You did not authorize the application

- The inquiry is duplicated

- The date or creditor is wrong

When you find an error, highlight it and write down:

- Which bureau report it is on (Equifax, Experian, or TransUnion)

- The account name and account number (use partial numbers if you prefer)

- Exactly what is wrong

- What the correct information should be

- What documents you have to support your claim

Step 3: Gather proof (make it easy to verify)

The bureaus and the company reporting the data (the “furnisher”) respond best to disputes that include clear documentation.

Helpful documents (include copies, not originals)

- Photo ID (driver’s license or state ID)

- Proof of address (utility bill, bank statement)

- Account statements showing the correct balance or payment

- Cancelled checks, confirmation emails, or payment screenshots

- Letters from the lender confirming a correction

- Police report or FTC Identity Theft Report (if identity theft is involved)

Tip: If you are sending a dispute by mail, label each attachment like “Attachment A,” “Attachment B,” and reference them in your letter. It sounds nerdy. It works.

Step 4: File your dispute (online or by mail)

You have two main routes: online disputes or mailed disputes. Both can work. The best choice depends on how complex the issue is and how much documentation you want to control.

Option A: Dispute online (fast and convenient)

Each bureau has an online dispute center. Online disputes are usually the quickest to submit and easiest to track.

- Good for: simple errors, straightforward accounts, quick corrections

- Downside: you may have limited space to explain, and the interface can push you toward checkboxes instead of a clear narrative

If you dispute online, still keep your own records:

- Take screenshots of the submission confirmation

- Save or print a copy of what you submitted

- Upload only the documents necessary to support the specific error

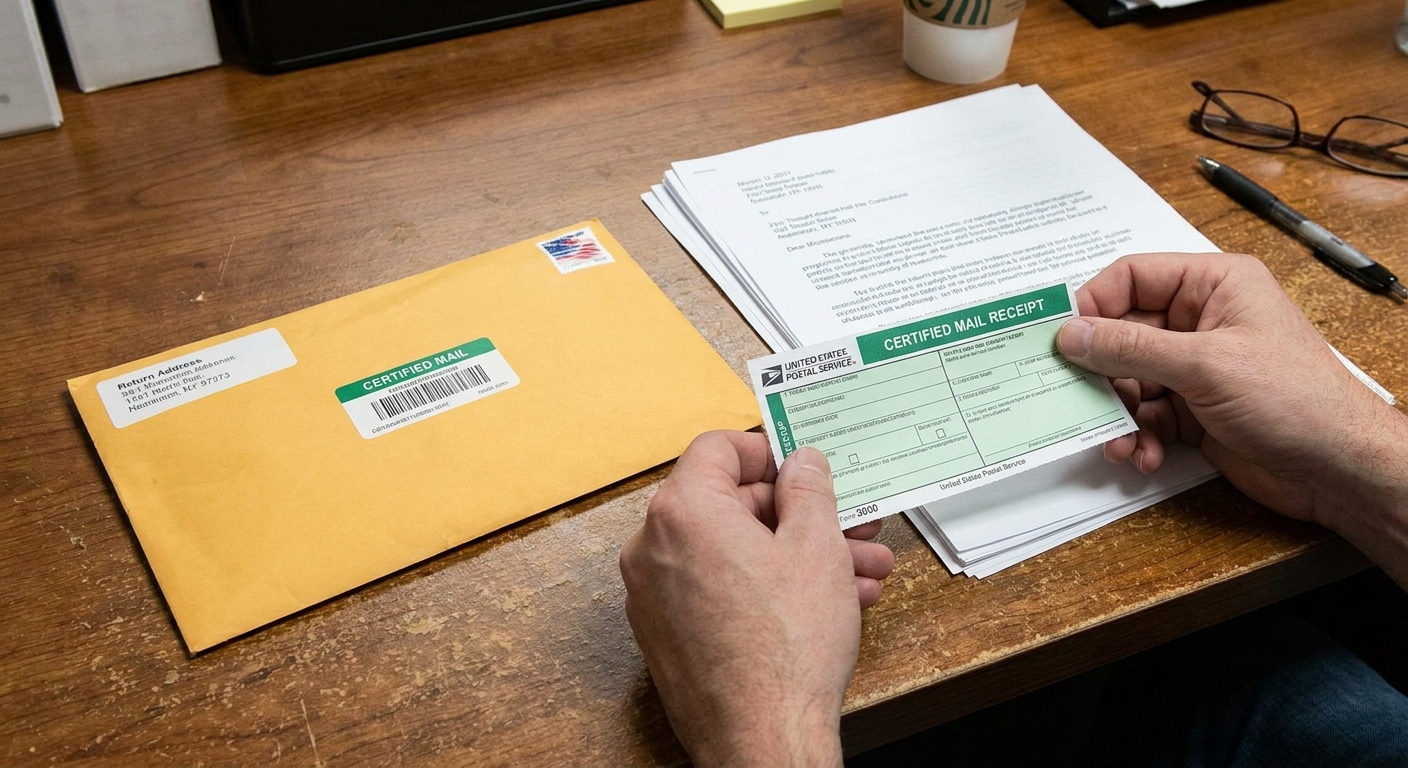

Option B: Dispute by mail (best for detailed disputes)

Mail gives you more control over your wording and paper trail.

- Good for: identity theft, mixed files, multiple errors, complicated timelines, or disputes that need explanation

- Best practice: send via certified mail with return receipt so you can prove the bureau received it

A simple dispute letter template (adapt as needed)

Keep it short, factual, and specific.

Your Name

Address

City, State ZIP

DateRe: Credit Report Dispute

To [Equifax/Experian/TransUnion],

I am writing to dispute inaccurate information on my credit report. The item(s) listed below are incorrect. Please investigate and correct or delete the inaccurate information.

Item being disputed: [Creditor/Collection Agency Name], Account #[partial]

What is wrong: [Example: Report shows 30-day late payment in May 2024]

What is correct: [Example: Payment was made on time on May 3, 2024]

Supporting documents: [Attachment A: bank statement showing payment; Attachment B: creditor statement]Please send me an updated copy of my credit report reflecting the results of your investigation.

Sincerely,

Your Name

Include copies of your ID and proof of address if requested or if the bureau needs to verify your identity.

Step 5: Also dispute directly with the company reporting it

Here is the part many people skip: the credit bureau is only one piece of the pipeline. The lender or collection agency that furnished the info can also correct it at the source.

You can send a similar dispute package directly to the furnisher (the bank, card issuer, auto lender, student loan servicer, or collection agency). Ask them to:

- Investigate the specific error

- Correct their reporting to all bureaus they report to

- Send you written confirmation of the correction

If the furnisher fixes it, the correction often updates across bureaus in the next reporting cycle, even if only one bureau had the dispute opened.

If identity theft is involved: protect your file

If the error is tied to identity theft (accounts you did not open, inquiries you did not authorize), do two things in parallel: dispute the items and lock down your credit so the problem does not keep spreading.

- Consider a fraud alert or a credit freeze. A fraud alert makes lenders take extra steps to verify it is you. A credit freeze helps prevent new credit from being opened in your name until you unfreeze.

- Get an Identity Theft Report. Filing an identity theft report through the FTC (and, if needed, a police report) can strengthen your disputes and help with certain legal protections.

This is not about panic. It is about cutting off the leak while you clean up the mess.

What happens after you submit: realistic timelines

Most credit report disputes are resolved within about 30 days after the bureau receives your dispute. Some disputes may take a bit longer depending on how the dispute was submitted, how quickly the furnisher responds, and whether the bureau needs more information from you.

Typical dispute timeline

- Day 1: You submit the dispute online or by mail.

- Days 1 to 7: Bureau logs it and sends it to the furnisher for investigation.

- Days 7 to 30: Furnisher investigates and responds.

- By around Day 30: Bureau completes investigation and sends results.

- After results: Your report updates, and you may see score changes shortly after.

Be patient, but not passive. Mark your calendar with the date the bureau received the dispute and the date you expect a response.

Understanding dispute results (and what to do next)

If the bureau corrects or deletes the item

Nice. Confirm the update on the report and save the results letter or email. Then:

- Check the other two bureaus to see if the same error exists there

- Consider setting a reminder to re-check in 30 to 60 days to make sure it does not reappear

If the bureau says the information was “verified”

This is frustrating, but it is not necessarily the end. Options include:

- Dispute again with stronger documentation. Make your dispute more specific and include clearer proof.

- Dispute directly with the furnisher if you have not already.

- Add a consumer statement to your report (short explanation). This does not fix the data, but it can add context for manual reviews. Use sparingly, since lenders may ignore it and it will not help your score.

- Request details. You can ask what was used to verify the information, especially if you believe they verified the wrong thing.

If an account is verified but you have strong evidence it is wrong, document everything and consider escalating through a formal complaint route.

Escalate: CFPB and state complaints

If you have done a clean dispute (specific claim, clear proof, good records) and you keep getting nowhere, escalation is less dramatic than it sounds. It is basically asking a regulator to lean on the process.

Option 1: File a complaint with the CFPB

You can file a complaint with the Consumer Financial Protection Bureau and attach your documentation. In many cases, the company has to respond, in writing, within a set timeframe.

- Where: consumerfinance.gov/complaint

- What to include: copies of your dispute letter(s), bureau results, proof documents, dates, and what you want (delete, correct, update dates, fix balance, remove late mark, and so on)

- Tip: Keep your “story” to a short timeline. One paragraph plus attachments beats three pages of frustration.

Option 2: Your state attorney general

If the issue is persistent or smells like unfair or sloppy behavior, your state attorney general may also be a good route. Many offices have online consumer complaint forms.

- What to include: same package as above, plus any pattern (for example, the same debt reappearing, or a furnisher refusing to correct an obvious error)

Escalation works best when you are calm, organized, and specific about what is inaccurate and what the correction should be.

Simple checklist: your dispute “go bag”

- Downloaded reports from Equifax, Experian, and TransUnion

- Highlighted errors and wrote a one-sentence description of each

- Created a list of what the correct info should be

- Copies of supporting documents (statements, receipts, letters)

- Copy of your ID and proof of address (if needed)

- Dispute letter (if mailing)

- Certified mail receipt and tracking number (if mailing)

- Screenshots and confirmation numbers (if disputing online)

- A calendar reminder for follow-up dates

Common mistakes that slow disputes down

- Disputing everything at once. Focus on the errors that matter most first, especially identity errors and accounts that are not yours.

- Being vague. “This is wrong” is harder to investigate than “This account shows a late payment on May 2024, but Attachment A shows payment on May 3, 2024.”

- Sending originals. Always send copies.

- Not keeping records. Save every letter, screenshot, and tracking number.

- Forgetting the furnisher. Fixing the source can prevent the error from coming back.

When professional help may be warranted

Most people can handle routine disputes themselves. That said, it may be worth talking to a qualified professional (like a consumer law attorney) if:

- You are dealing with identity theft and multiple fraudulent accounts

- Your file appears mixed with someone else’s information

- The same verified error keeps reappearing after being corrected

- You have documentation, but the bureaus and furnishers keep ignoring it

- You are facing an urgent lending deadline and need coordinated, precise action

If you go this route, look for someone who explains your options clearly and does not promise guaranteed score increases. No one can honestly guarantee that.

FAQ

Will disputing hurt my credit score?

Filing a dispute does not directly hurt your score. If an inaccurate negative item is corrected or removed, your score may improve. If the item is accurate and remains, your score may stay the same.

How long do negative items stay on a credit report?

Many negative items stay for about seven years, but the exact timeline depends on the type of item and the reporting rules. If you think something is too old to be reported, dispute it and reference the relevant dates you can document.

Should I dispute online or by mail?

Online is fine for simple issues. Mail is often better for complicated situations because you can include a clean paper trail and control your wording.

What if the error is on only one bureau?

Dispute it with that bureau. Then check the other two anyway. A lot of people discover the same mistake is showing up in more than one place.

Bottom line

Disputing credit report errors is not about gaming the system. It is about making sure your file reflects reality. Pull your reports, document the specific mistake, send a clear dispute with proof, and follow up like you would with any important paperwork.

If you want the easiest next step: set a 45-minute timer, pull all three reports, and write down the top three items that look off. That alone puts you ahead of most people.