If paying for college feels like a maze, you are not alone. The FAFSA is one of those forms that sounds simple until you are in the middle of it, bouncing between logins, tax info, and “contributor” invites. The good news is that most FAFSA delays are predictable, and with a little prep you can avoid the stuff that jams up aid.

This guide covers what to do before you sit down to file FAFSA 2026, what documents you actually need, how deadlines work, what changed (hello, SAI), and the mistakes I see most often that slow down financial aid.

FAFSA 2026 quick timeline

FAFSA timing matters because many states and schools give out certain aid on a first-come, first-served basis. That means “earlier” can equal “more money,” even if your federal eligibility would be the same later.

When can you file FAFSA 2026?

FAFSA cycles are named for the school year they cover. FAFSA 2026 refers to the 2026–27 school year. The Department of Education typically opens each FAFSA in the fall, but exact launch dates can vary by year due to system updates.

- Best move: Check the Federal Student Aid site in late summer and early fall and plan to file as soon as the application is available.

- Do not wait for acceptance letters: You can list schools before you are admitted and update your list later.

Which tax year does FAFSA 2026 use?

FAFSA uses the “prior-prior year” rule. For the 2026–27 FAFSA, that usually means you will reference 2024 federal tax information. Even though the FAFSA may pull data directly from the IRS (with consent), it still helps to know which return you are working off of so you can spot issues quickly.

Deadlines that actually matter

There is no single deadline. There are three layers, and the earliest one should be your target:

- Federal deadline: The last date the federal government accepts the FAFSA for the award year.

- State deadline: Often much earlier, and some states run out of funds.

- College deadline: Set by each school and can be tied to admission, scholarships, or priority aid windows.

My rule of thumb: Treat your state and top-choice school “priority” date as the real deadline, not the federal one.

Before you start: build your “FAFSA folder”

FAFSA goes faster when you are not hunting down passwords and PDFs mid-application. Set up a folder on your computer or Google Drive and drop everything in one place.

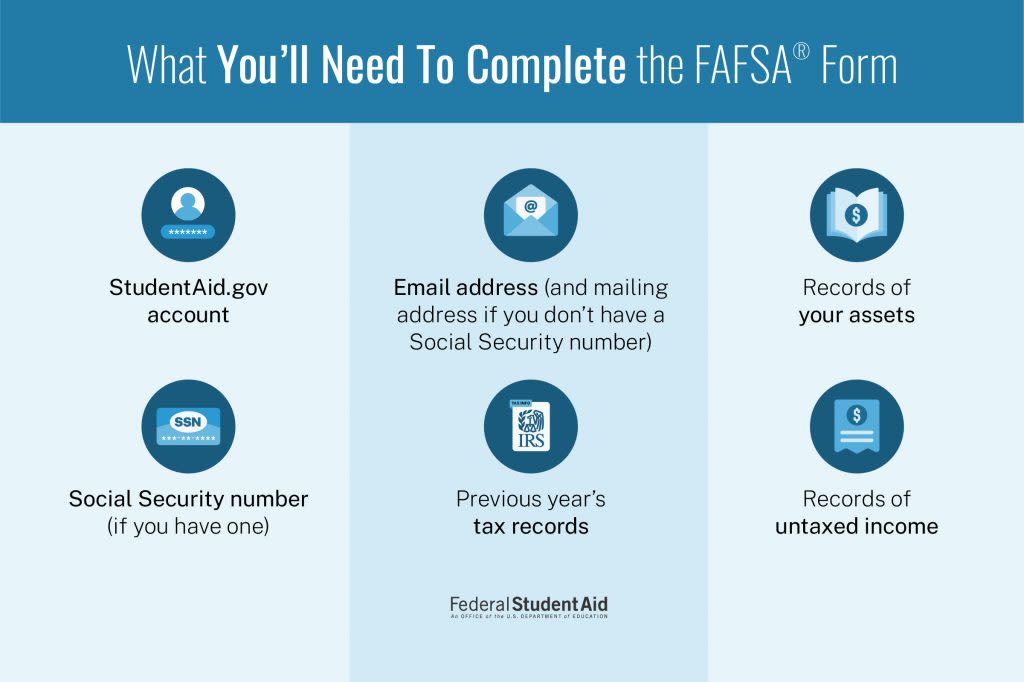

Documents and info you will want handy

- Social Security numbers for the student and any required contributors (or Alien Registration Number if applicable).

- Date of birth and legal name exactly as shown on Social Security card.

- Current address and contact info.

- Driver’s license number (if requested).

- 2024 federal tax information for the 2026–27 FAFSA (often pulled via IRS data sharing when you consent, but still good to have your return for reference).

- Records of untaxed income if applicable (examples can include child support received or certain veterans benefits).

- Bank account balances as of the day you file.

- Investment and asset info if applicable (non-retirement investments, certain businesses or farms depending on FAFSA rules).

- List of schools you may apply to (you can adjust later).

Two reminders that reduce stress: you typically do not report retirement accounts like a 401(k) or IRA as assets, and a primary home is generally not reported as an asset on the FAFSA. When in doubt, follow FAFSA prompts exactly and do not “freestyle” extra information.

SAI: the number FAFSA uses now

If you filed FAFSA in past years, you may remember the Expected Family Contribution (EFC). FAFSA now uses the Student Aid Index (SAI) instead. You will still see it used as a key input for aid decisions, but the label changed and the formula was updated.

Quick translation: If you are used to “EFC,” think “SAI” as the current version of that concept.

Contributors: who and why

In recent FAFSA updates, the term contributor became a big deal. A contributor is someone who is required to provide information on the FAFSA, and they may need to log in and provide consent for IRS data sharing.

Who counts as a contributor?

It depends on the student’s dependency status and the parents’ marital and living situation. Common examples:

- The student is always involved.

- A parent (or parents) may be contributors for dependent students.

- A spouse may be a contributor for a married student, and sometimes for a parent contributor as well.

If your family situation is complicated, do not guess. Use the dependency questions inside FAFSA, and if needed, call the financial aid office of your target school. They would rather answer questions now than unwind an incorrect submission later.

Create your account IDs early

Each required person may need their own Federal Student Aid (FSA) ID. Create these well before you plan to file, because identity verification and account recovery are common time-sinks.

- Use the person’s legal name exactly.

- Make sure each person has access to the email and phone number on their account.

- Store passwords in a password manager so you are not locked out on filing night.

IRS data consent: do not skip it

FAFSA may request consent to pull tax information directly from the IRS. In many situations, consent is required to complete the FAFSA and be considered for aid.

What to know about consent

- Consent is required for each contributor who is asked to provide it, even if they did not earn enough to file a tax return.

- If a required contributor does not provide consent, the FAFSA may not be processed for aid eligibility the way you expect. In plain English: it can stop you cold.

Why consent matters

- It reduces manual entry errors.

- It can reduce the odds of verification issues later.

- It speeds up processing because the data matches what the IRS has on file.

Common consent problems that cause delays

- A contributor does not complete their portion of the FAFSA.

- A contributor cannot access their FSA ID, so they never get to the consent step.

- The contributor’s name or SSN does not match Social Security records, causing identity friction.

Bottom line: If someone is a required contributor, they need to participate promptly. Treat it like a group project with a real deadline.

Your school list strategy

Many people treat the school list like a throwaway step. It is not. Listing a school is how you authorize your FAFSA information to be sent to that school.

How to build a smart list

- Start with your top choices and any schools with earlier priority aid deadlines.

- Add at least one financial “safety” school you would actually attend if the aid offer is strong.

- Include in-state public options if cost is a major factor, since state aid can be tied to state schools.

Can schools see the other schools on your list?

No. Schools receive your FAFSA information for their school, but they cannot see the other schools you list on your FAFSA. So you can build your list based on deadlines and real interest without worrying that colleges are comparing notes.

Prep plan for one evening

If you want a simple plan, here is the exact order I would follow.

- Make a contributor checklist: student, parent 1, parent 2 if applicable, spouse if applicable.

- Create or verify each FSA ID: confirm everyone can log in successfully.

- Open your FAFSA folder: 2024 tax return (for reference), bank balances, untaxed income notes, school list.

- Pick a filing night: 45 to 60 minutes when all contributors are reachable.

- File and submit: do not leave it in “draft.”

- Save confirmations: download or screenshot the submission confirmation page.

Mistakes that delay aid

These are the issues that most often lead to processing delays, corrections, or verification headaches.

1) Mismatched names, SSNs, or dates of birth

FAFSA is picky because it has to match federal records. Use legal names, and double-check digits before you hit next.

2) Contributors do not finish their section

One person forgetting to log in can hold up the entire submission. If you are the student, follow up like you are scheduling a dentist appointment. Be politely persistent.

3) Guessing on assets or income

If you are not sure, pause and look it up. A wrong number can trigger verification or require corrections later. For bank accounts, use the balance as of the day you file.

4) Skipping IRS data consent

If the system requests consent, take it seriously. It is not just a convenience feature. Each required contributor should complete it, even if they did not file taxes.

5) Submitting too late for state or school priority aid

You can submit a perfect FAFSA and still miss out on money because funds ran out. This is why “file early” is not just generic advice.

6) Ignoring emails from the school

After your FAFSA is processed, a college may request documents. If you ignore those requests, your aid can stall even though you did everything right on the FAFSA itself.

Verification: do not panic

Verification is when a school asks you to prove certain FAFSA information. It is common and it does not automatically mean you did something wrong. Think of it like getting flagged for extra screening at the airport.

What can trigger verification?

- Information that does not match other records.

- Large changes year over year.

- Commonly misreported fields like household size or certain income items.

- Random selection.

How to get through verification faster

- Respond quickly: delays here can delay your aid disbursement.

- Send exactly what is requested: not extra documents, not partial screenshots.

- Keep copies: save PDFs of what you submit.

- Ask questions early: if a request is confusing, call the financial aid office.

If your finances changed

The FAFSA is built on past tax data, but life happens. If your family income dropped, a parent lost a job, medical bills spiked, or there was a separation or divorce, you may be able to request a review from the school.

Ask about a professional judgment review

Schools may adjust certain FAFSA-related figures based on documented special circumstances. This is not automatic and it is not guaranteed, but it is absolutely worth asking about if your current reality is very different from the tax year used.

Tip: Keep documentation like termination letters, unemployment statements, medical bills, or a written explanation of the change. The financial aid office will tell you what they can accept.

529 plans and “Roth for college”

I love a good college savings strategy, but the FAFSA is the application stage where planning meets reality. A few quick, practical notes:

- Do not move money around impulsively right before filing. Asset reporting rules are specific, and last-minute transfers can create confusion.

- Keep clean records for education accounts. If a school requests verification, you want statements that make sense.

- Plan for cash flow, not just totals. Even with aid, you may have timing gaps before refunds or disbursements hit.

If you are already saving in a 529 or considering a Roth IRA strategy, that is great. Just treat FAFSA as its own project with a checklist and a calendar.

FAFSA 2026 checklist

- Create and test FSA IDs for all contributors

- Confirm legal names, SSNs, and dates of birth match records

- Prepare 2024 tax return (for reference), bank balances, and untaxed income notes

- Decide your school list with priority deadlines in mind

- File as soon as the FAFSA opens

- Submit and save confirmation

- Watch for school emails about next steps or verification

If you want the most “boring” FAFSA season possible, the secret is simple: get the IDs done early, get contributor cooperation lined up, consent to IRS data sharing, and file before the priority deadlines. That is how you avoid the delays that make college funding feel harder than it has to be.