If you are reading about bankruptcy, chances are you are not doing it for fun. You are doing it because the math is not working anymore and the stress is starting to leak into everything else. I have been in the “how did it get this bad?” headspace before, and while my own path was a debt payoff grind instead of bankruptcy, I can tell you this: understanding your options clearly makes the fear shrink.

The two most common consumer bankruptcies are Chapter 7 and Chapter 13. Chapter 7 is often called “liquidation.” Chapter 13 is often described as a “repayment plan” (you may also hear it called “reorganization” shorthand). Those labels are accurate enough, but they are not very helpful until you translate them into normal-language questions like:

- How long will this take?

- How much will it cost up front?

- Will I lose my car or my house?

- Which debts get wiped out, and which ones will follow me anyway?

- What happens to my credit, realistically?

Let’s walk through those, step by step, without the legal jargon overload.

Key takeaways (for skimmers):

- Chapter 7 is usually faster (often months) and wipes out many unsecured debts, but non-exempt assets can be at risk.

- Chapter 13 is a 3 to 5 year repayment plan that can help you keep property and catch up on mortgage or car arrears.

- Both chapters usually trigger an automatic stay, but repeat filings and certain situations (like some evictions) can limit it.

- Some debts usually survive either way (student loans in most cases, child support, many taxes, fines, restitution).

Quick definitions

Chapter 7: wipe out eligible debts

In a Chapter 7 bankruptcy, you are asking the court to discharge eligible debts after a review of your finances. In exchange, a court-appointed trustee can sell certain non-exempt assets (property not protected by exemption laws) to repay creditors.

Many Chapter 7 cases are “no-asset” cases, meaning there is nothing non-exempt worth selling. But asset risk is still part of the deal, and it depends heavily on your state exemptions and what you own.

Chapter 13: repay some debts over time

In a Chapter 13 bankruptcy, you keep your property and agree to a court-approved repayment plan , usually over 3 to 5 years. After you complete the plan, remaining eligible unsecured debts can be discharged. Chapter 13 is commonly used by people who have steady income, are behind on a mortgage or car, or do not qualify for Chapter 7 due to income or other factors.

Costs

Bankruptcy costs vary by state, complexity, and attorney, but there are a few consistent buckets: court filing fees, credit counseling courses, and legal fees (if you hire an attorney, which most people do). Court fees can change over time, so treat any numbers as approximate and confirm your local court’s current fee schedule.

Chapter 7 costs

- Court filing fee: often in the mid-hundreds of dollars (commonly around the $300 to $400 range).

- Required courses: two courses (credit counseling before filing and a debtor education course after filing), often roughly $10 to $50 each depending on provider and fee waivers.

- Attorney fees: vary widely by market and complexity. In Chapter 7, fees are often paid mostly up front because the case moves quickly.

If cash is tight, that up-front nature is a real issue. Some courts allow filing fee installments or fee waivers in limited cases, and some attorneys offer payment options, but it depends.

Chapter 13 costs

- Court filing fee: often in the mid-hundreds of dollars (commonly around the $300 to $400 range).

- Required courses: same two courses as Chapter 7.

- Attorney fees: vary, but are often structured so part is paid up front and the rest is paid through the repayment plan (subject to local rules and court approval).

So while Chapter 13 can involve higher total legal costs in some cases, it can be more manageable because the fees are frequently spread out.

Important: I am not your attorney, and this is not legal advice. Ask a local bankruptcy attorney for a written fee quote that includes what is and is not covered (amendments, extra hearings, creditor disputes, and so on).

Timelines

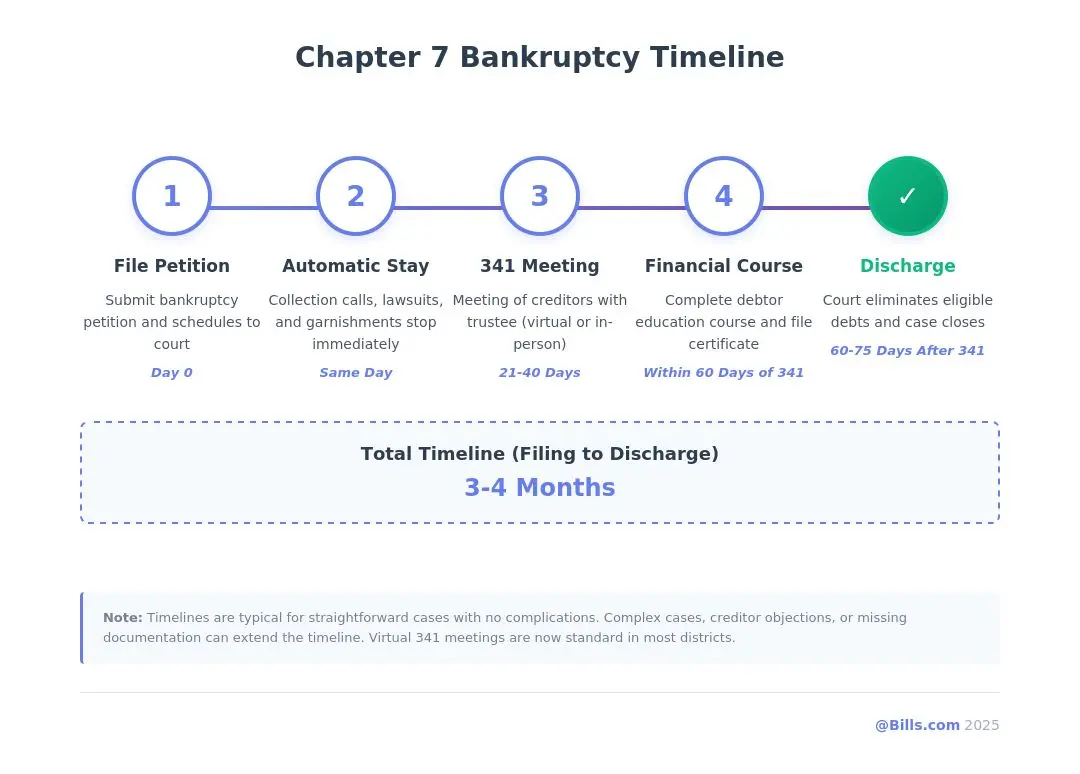

Chapter 7 timeline

A typical Chapter 7 case is often completed in about 3 to 6 months from filing to discharge, assuming it is straightforward. If there are non-exempt assets to administer, a creditor dispute, or an adversary proceeding (for example, a fight about dischargeability), the case can take longer.

The steps usually include:

- Complete the pre-filing credit counseling course.

- File your petition and schedules.

- Automatic stay begins.

- Attend the “341 meeting” (a short meeting with the trustee).

- Complete the debtor education course.

- Receive discharge if everything checks out.

Chapter 13 timeline

Chapter 13 is a longer commitment. After filing, you propose a repayment plan and start making payments, often within about a month. Many plans last:

- 3 years (often when income is below the state median)

- 5 years (often when income is above the state median)

Your discharge generally happens after you complete the plan and meet other requirements. A common one people overlook is that you usually must stay current on domestic support obligations (child support or alimony) and meet required filing and documentation rules.

Automatic stay

Both Chapter 7 and Chapter 13 typically trigger an automatic stay when you file, which generally pauses collection activity such as:

- Debt collection calls and letters

- Most lawsuits and wage garnishments

- Many foreclosures and repossessions (at least temporarily)

There are exceptions, and some creditors can ask the court to lift the stay. Certain actions, like many family court matters, can continue.

Two important nuances:

- Repeat filings can limit the stay. If you have filed bankruptcy recently, the stay may be limited (for example, only 30 days) or may not go into effect at all unless you ask the court and meet specific requirements.

- Evictions can have special rules. Some eviction situations are not fully stopped by the stay, especially if a landlord already has a judgment for possession. If you are facing eviction, talk to a local attorney immediately.

For many people, the automatic stay is the first deep breath they have taken in months.

Exemptions and assets

This is the part everyone worries about, and it is also where details matter a lot. Exemptions are laws that protect certain property up to a specific value.

Exemptions can be based on federal rules or your state’s rules, depending on where you file. Some states require you to use the state exemption system and do not allow federal exemptions. This is one of the biggest reasons local advice matters.

Chapter 7 and asset risk

In Chapter 7, the trustee can sell non-exempt property and use the proceeds to repay creditors. In practice, many people who file Chapter 7 have mostly exempt property, such as:

- Basic household goods

- Clothing

- Some amount of vehicle equity

- Retirement accounts that are protected under applicable law

- Tools needed for work (up to limits)

What tends to create risk is significant equity in a home or car beyond the exemption limit, valuable collections, or substantial non-retirement investment accounts.

Chapter 13 and keeping property

Chapter 13 is often chosen when someone wants to keep assets that might be at risk in Chapter 7. You usually keep your property, but you must follow the plan and make payments. Your plan amount can be influenced by what creditors would have received in a Chapter 7 liquidation.

Eligibility

Chapter 7 and the means test

To qualify for Chapter 7, many filers must pass a “means test,” which compares your income and certain allowed expenses to determine whether you have enough disposable income to repay creditors. If your income is below the median for your state and household size, you may qualify more easily. If it is above, you may still qualify, but the calculation gets more detailed.

Also, bankruptcy law includes waiting periods between discharges if you have filed before. If you have a prior bankruptcy, tell your attorney up front so you do not get surprised by timing rules.

Chapter 13 needs steady income

Chapter 13 generally requires that you have enough reliable income to make plan payments. It can be a fit if you are behind on secured debts like a mortgage or car loan and need time to catch up, or if you do not qualify for Chapter 7.

Which debts get discharged?

Here is the simplest way to think about it: both chapters can wipe out many unsecured debts, but some debts typically survive bankruptcy no matter what chapter you file.

Commonly discharged in both chapters

- Credit card balances

- Medical bills

- Personal loans (unsecured)

- Old utility bills

- Many collection accounts

- Some older income tax debts (only if strict rules are met)

Often not discharged

- Most student loans (unless you win an undue hardship case, which is possible but challenging)

- Child support and alimony

- Many recent income taxes (older taxes can be dischargeable only under specific timing and filing rules)

- Tax liens (even when the underlying tax debt may be dischargeable, the lien can survive against the property)

- Court fines and criminal restitution

- Debts from fraud or certain intentional misconduct (if a creditor successfully challenges dischargeability)

One more practical warning: certain luxury purchases or large cash advances shortly before filing can be presumed non-dischargeable, depending on the timing and facts. If you are considering bankruptcy, stop playing games with credit cards and get real advice before you do anything that creates extra risk.

Secured debts: the special category

Your mortgage and car loan are secured by collateral. Bankruptcy may discharge your personal liability on some secured debts, but it does not erase the lender’s right to repossess or foreclose if you do not pay.

In plain English:

- If you want to keep the house or car, you generally need to stay current and meet whatever your lender and local practice require. In some places and with some lenders, that may include a reaffirmation agreement. In others, staying current may be enough.

- If you want to give up the collateral, bankruptcy can often help you walk away from the remaining balance.

How Chapter 13 helps with arrears

One big Chapter 13 advantage is the ability to catch up on missed payments over time through the plan, especially for mortgages. This is a common reason people choose Chapter 13 even if Chapter 7 sounds more appealing.

Co-signers

If someone co-signed a debt with you, bankruptcy can get tricky. Chapter 7 generally does not protect your co-signer from collection if the debt is discharged as to you. Chapter 13 can offer a “co-debtor stay” for certain consumer debts, but it has rules and exceptions. If a co-signer is involved, bring that up early in any consult.

Credit impact

Bankruptcy is a major credit event. It will likely lower your score in the short term, especially if your credit was decent before filing. If your credit is already bruised from missed payments, charge-offs, and collections, the score drop might be smaller than you expect.

How long it can report

- Chapter 7: can remain on your credit report for up to 10 years from the filing date.

- Chapter 13: is commonly reported for up to 7 years, typically from the filing date. Reporting practices can be a point of confusion, so focus on the practical takeaway: it is a long-term mark, but it is not permanent.

What recovery comes down to

Your post-bankruptcy credit rebuild is usually driven by a few boring but powerful habits:

- Pay every remaining obligation on time (housing, car, utilities, insurance).

- Keep credit usage low if you use a card again.

- Build cash buffers so emergencies do not go back on plastic.

- Check your reports to make sure discharged debts are updated correctly.

If you are chasing financial peace, bankruptcy is not “the end.” It is a reset button with consequences. The win is what you do with the clean slate.

Chapter 7 vs Chapter 13

Chapter 7 tends to fit when

- You have limited income and little ability to repay.

- Most of your debt is unsecured (credit cards, medical).

- You do not have significant non-exempt assets at risk.

- You want the fastest route to discharge.

Chapter 13 tends to fit when

- You have steady income and can commit to a plan.

- You are behind on your mortgage or car and want time to catch up.

- You have assets you want to protect that could be vulnerable in Chapter 7.

- You do not qualify for Chapter 7.

Bankruptcy vs other options

On Smart Cent Guide we talk a lot about debt management plans, debt settlement, and consolidation loans. Bankruptcy is different because it is a legal process with court protection and potential discharge of eligible debts.

As a high-level gut check:

- If you can realistically repay your debts within a few years with a structured plan and reduced interest, a non-bankruptcy option may be worth exploring.

- If you cannot repay even with reduced interest, are facing lawsuits or garnishment, or your debt load is wildly out of proportion to income, bankruptcy may be the more honest solution.

The right move is the one that ends the cycle and lets you stay housed, insured, and functional.

Questions to ask an attorney

Even if you are leaning strongly toward one chapter, a short consult can save you from expensive surprises. Consider asking:

- Which exemptions apply in my state, and what property is at risk in Chapter 7?

- Am I allowed to use federal exemptions, or does my state require state exemptions?

- Do I pass the means test for Chapter 7?

- If I file Chapter 13, what would my estimated monthly plan payment be?

- Can Chapter 13 help me catch up on mortgage or car payments?

- Which of my debts are likely dischargeable, and which are not?

- How will taxes, refunds, or a pending inheritance affect the case?

- How do co-signed debts work in my situation?

- What is your total fee, and what is included?

The bottom line

Chapter 7 is usually faster and built to eliminate eligible unsecured debts, but it can put non-exempt assets at risk. Chapter 13 is a longer repayment plan that can help you protect property and catch up on secured debts, with eligible remaining balances discharged after you complete the plan.

If you are feeling paralyzed, pick one small next step: pull your credit reports, list your debts with balances and interest rates, and schedule a consult with a local bankruptcy attorney. Clarity is the first real form of relief.

Disclosure: This article is for educational purposes and is not legal advice. Bankruptcy rules vary by state and your specific situation.