If you have ever tried to contribute to a Roth IRA and hit the income limit wall, you have probably heard someone casually say, “Just do a backdoor Roth.”

That advice can be solid. It can also get expensive if you ignore one very specific landmine: the pro-rata rule.

This guide breaks the backdoor Roth IRA down like a real-life checklist: what it is, who it is for, the step-by-step flow, how Form 8606 fits in, timing details people miss, and the most common reasons to skip it. This is educational info, not personalized tax advice.

What a backdoor Roth IRA is

A backdoor Roth IRA is not a special account. It is a two-step process people use to get money into a Roth IRA when their income is too high for a direct Roth contribution.

The two steps

Contribute to a Traditional IRA as a non-deductible contribution (meaning you do not take a tax deduction for it).

Convert that Traditional IRA money to a Roth IRA.

The basic idea is simple: if you cannot contribute directly to a Roth, you contribute to a Traditional IRA and then convert it.

Where it gets tricky is how taxes are calculated during the conversion, especially if you already have pre-tax IRA money elsewhere.

Why people use it

Roth IRAs have income-based eligibility rules. At higher incomes, direct Roth contributions get reduced and eventually phased out.

That is the whole “why” behind the backdoor Roth. It is a workaround for the contribution limit rules, not a hack to avoid taxes that you legitimately owe.

Important: Your workplace plan (like a 401(k)) has separate rules. A backdoor Roth IRA is about IRA contribution limits, not whether you can contribute to your 401(k) or do a Roth 401(k).

Because phaseout ranges and limits change over time, confirm the current year’s Roth IRA income limits and IRA contribution limits on IRS guidance (or a trusted tax site) before you contribute.

Who it is for

The backdoor Roth IRA tends to fit best if most of the following are true:

You earn too much to contribute directly to a Roth IRA.

You have the cash flow to contribute up to the annual IRA maximum (plus catch-up if you qualify).

You want more money growing tax-free long term.

You have little to no pre-tax money sitting in Traditional, SEP, or SIMPLE IRAs (this is the big one).

It can also make sense if you want more flexibility later. Roth dollars can be powerful in retirement planning because qualified Roth withdrawals are generally tax-free (think: rules like the 5-year clock and age 59½ or another qualifying event).

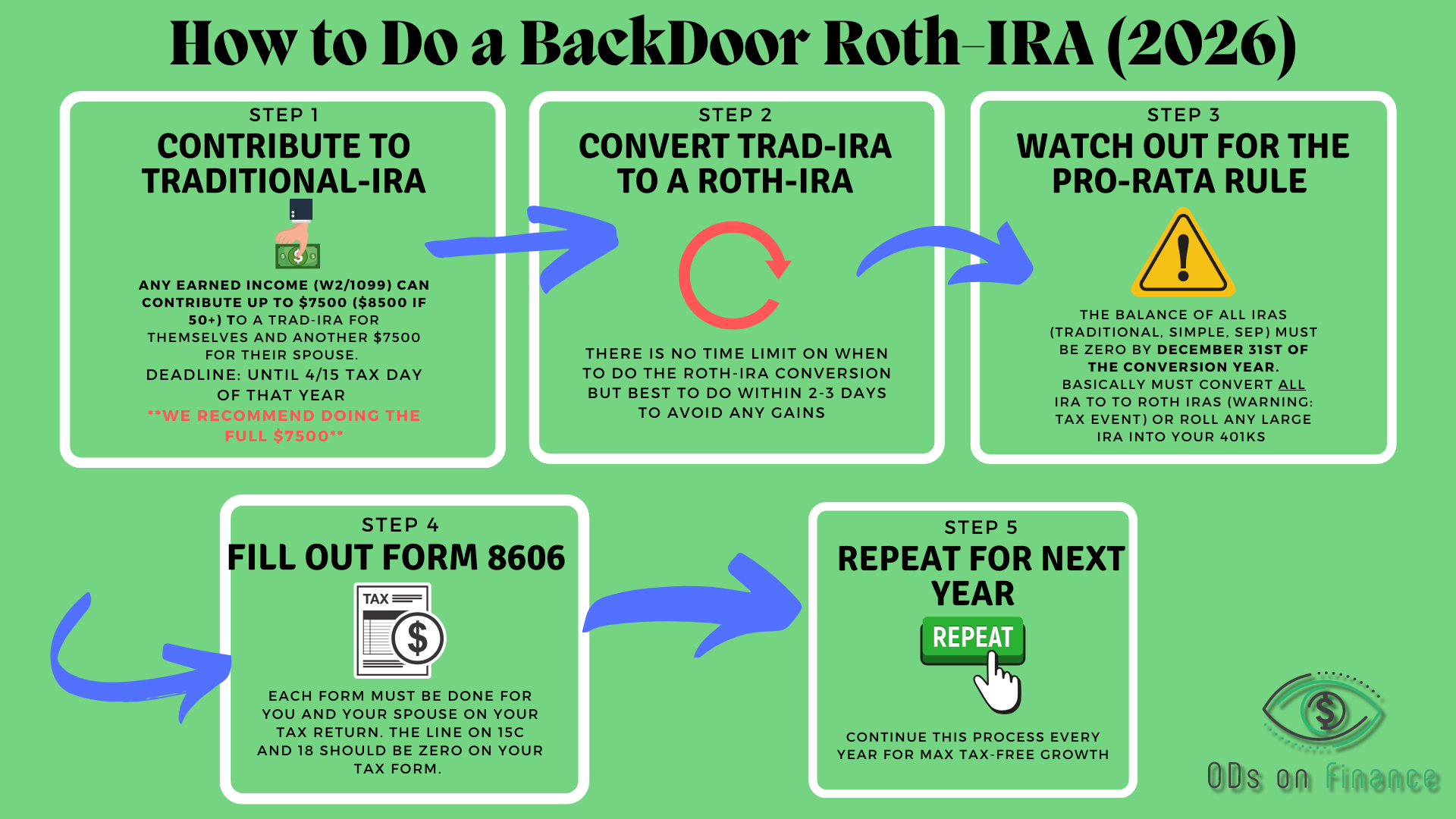

Step-by-step flow

Here is the straightforward flow many people follow when they are trying to avoid accidental taxes and paperwork headaches. The details can vary by brokerage, but the sequence is what matters.

1) Open the right accounts

A Traditional IRA (if you do not already have one)

A Roth IRA (if you do not already have one)

2) Make a non-deductible Traditional IRA contribution

Contribute cash to the Traditional IRA and intentionally do not take a deduction for it. This creates “basis,” meaning after-tax money inside the IRA.

Many people leave the contribution in a settlement fund or cash temporarily to minimize any gains between contribution and conversion.

3) Convert to Roth IRA

Next, convert from the Traditional IRA to the Roth IRA.

In practice, you are converting whatever amount you choose (often the full available balance you just contributed). If the value moved between contribution and conversion, that shows up in the math:

If it grew, the growth is typically taxable when converted.

If it fell, you are converting a lower value, which usually means less (or no) taxable amount on that portion, depending on your basis and pro-rata situation.

4) Invest inside the Roth IRA

Once the funds land in the Roth IRA, you invest according to your plan (index funds, target-date funds, whatever fits your strategy and risk tolerance).

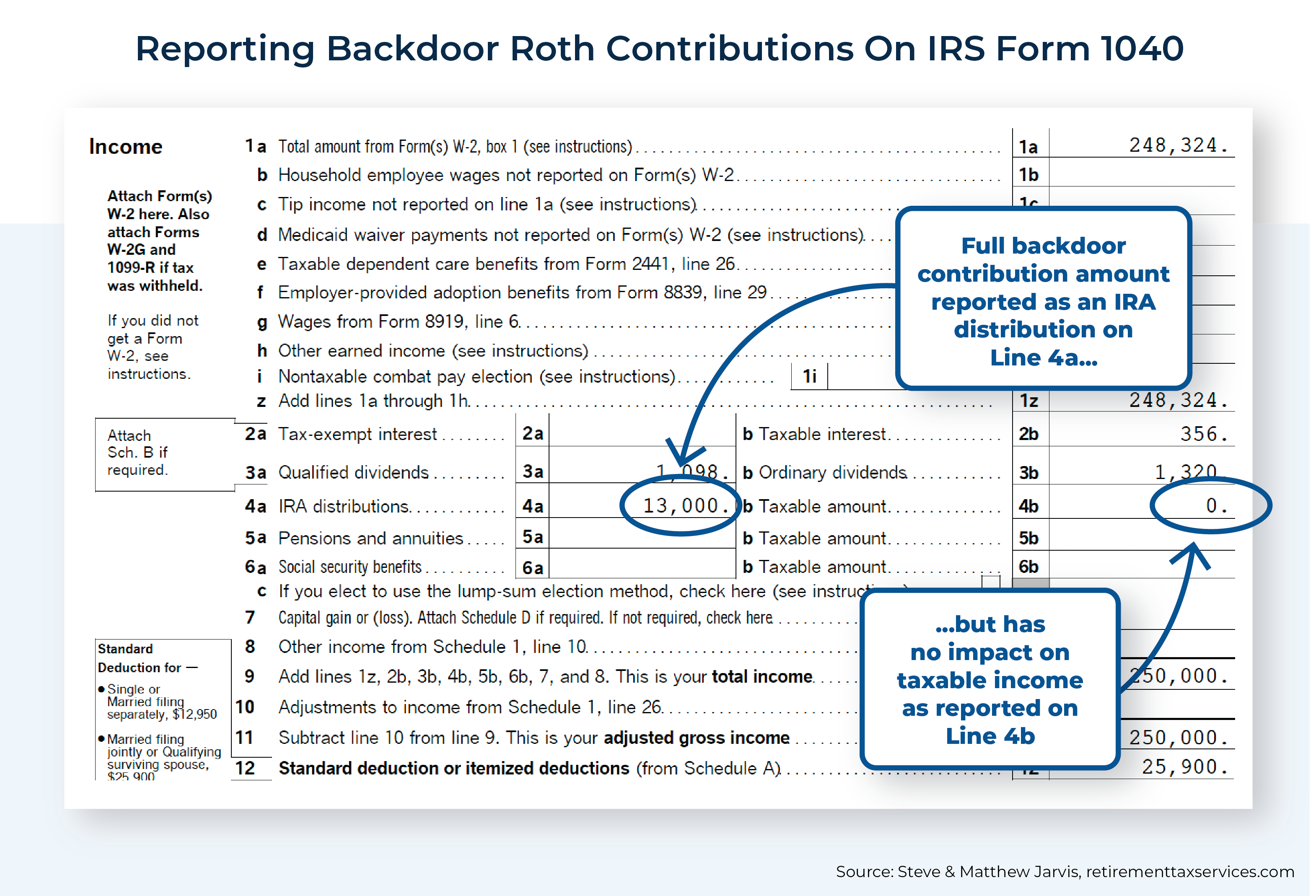

5) File Form 8606 with your taxes

This is the paperwork piece that tells the IRS, “Hey, that Traditional IRA contribution was after-tax, so do not tax me on it again.” More on this below.

Timing rules people miss

Contribution deadline

Traditional IRA contributions for a given tax year can generally be made up to the tax filing deadline (usually in April). Your brokerage will typically ask which tax year the contribution is for.

Conversion timing

Roth conversions are taxable based on the calendar year in which the conversion happens. So a contribution for last year made in early April can still be converted in the current year, but the conversion goes on the current year’s tax return.

Do you have to wait?

There is no official IRS waiting period between contribution and conversion. Many people convert soon after the contribution posts to limit gains. Brokerages may have processing times.

Form 8606 basics

Form 8606 is how you track non-deductible (after-tax) contributions to Traditional IRAs and how much of a conversion should be taxable.

At a high level, it does two jobs:

Reports your non-deductible contribution so the IRS knows you already paid tax on that money.

Calculates the taxable portion of your conversion using your total IRA picture and your after-tax basis.

Lay-level example

Say you contribute $7,000 to a Traditional IRA and you do not deduct it. Then you convert that amount to a Roth IRA.

If you have no other Traditional, SEP, or SIMPLE IRA balances and the money did not grow, the conversion is usually close to non-taxable.

Form 8606 is what supports that outcome on your tax return.

Do not skip Form 8606. Even if your tax software “seems” to handle it, you still want to confirm it is included and correct. If the IRS does not see your basis tracked properly, you can end up effectively paying tax twice on the same dollars.

The pro-rata rule

Here is the part that trips people up.

When you convert money from a Traditional IRA to a Roth IRA, the IRS does not let you choose to convert “only the after-tax dollars.” Instead, your conversion is treated as a proportional mix of:

After-tax basis (non-deductible contributions)

Pre-tax IRA money (deductible contributions and earnings)

This is called the pro-rata rule.

Why it matters

If you have a large rollover IRA from an old 401(k), or you have years of deductible Traditional IRA contributions, your “simple” backdoor Roth conversion can become partially taxable. Sometimes very taxable.

A simple pro-rata example

Imagine you have:

$93,000 in pre-tax Traditional IRA money (rollovers, deductible contributions, growth)

$7,000 in after-tax basis you just contributed

Total IRA money considered in the pro-rata calculation: $100,000.

If you convert $7,000, only about 7% of that conversion is treated as after-tax. The other ~93% is treated as pre-tax and gets taxed as ordinary income.

That is the “wait, I thought this was tax-free?” moment.

What balances count (and when)

The pro-rata rule looks at your combined balances across:

Traditional IRAs

SEP IRAs

SIMPLE IRAs

It also factors in activity during the year. The Form 8606 calculation uses your year-end fair market value (as of December 31) along with IRA distributions and conversions during the year to determine what portion is taxable.

One common misconception: a separate Traditional IRA account does not “isolate” after-tax dollars. The IRS treats these IRA types as one big bucket for this math.

Also helpful to know what does not count in the IRA pro-rata bucket: 401(k), 403(b), and TSP accounts (workplace plans follow different rules).

Note: Inherited IRAs can follow different rules and tax treatment, so do not assume the backdoor playbook applies the same way there.

How people avoid pro-rata

This is where planning matters, and where it can be smart to pull in a tax pro if you are unsure.

Option A: Roll pre-tax IRA money into a 401(k)

If your current employer’s 401(k) plan accepts roll-ins, you may be able to move pre-tax IRA money (like a rollover IRA) into the 401(k). 401(k) balances are not counted in the IRA pro-rata rule.

This can “clear the runway” so future backdoor Roth conversions are cleaner.

Two important fine-print items:

Most workplace plans only accept pre-tax money. Your after-tax basis usually cannot be rolled into a 401(k).

Not all plans allow roll-ins, and not all IRA dollars are eligible, so confirm with your plan administrator before moving anything.

Option B: Convert more, intentionally

Some people decide to convert a larger amount and pay the tax now, especially if they are in a lower tax year (career break, relocation, business loss, etc.). This is less of a “backdoor contribution” and more of a deliberate Roth conversion strategy.

Option C: Skip it

Sometimes the simplest answer is: do not force it this year.

When to skip

I love a good money move, but not every money move is a good move for your situation. Consider skipping (or pausing) a backdoor Roth IRA if any of these are true:

You have significant pre-tax money in Traditional, SEP, or SIMPLE IRAs and you cannot or do not want to roll it into a 401(k). The pro-rata rule can make the conversion meaningfully taxable.

You are not confident you will file Form 8606 correctly. This is fixable, but it is not optional.

You need the money soon. Roth IRAs are best used for long-term retirement goals, not near-term spending.

You are dealing with complicated tax items (business losses, large capital gains, multi-state issues) and you are not working with a tax professional. The conversion could bump you into higher tax impacts beyond just the conversion itself.

You are eligible for a direct Roth contribution anyway. If you can contribute directly, do that and keep life simple.

If you skip it, you still have strong options: maxing a 401(k), using an HSA if eligible, or focusing on taxable investing with a clean, low-cost index fund strategy.

Common mistakes

Forgetting Form 8606 or filing it wrong (especially if you have prior-year basis).

Ignoring your December 31 IRA balances and then being shocked by the pro-rata result.

Trying to fix pro-rata after the fact, like rolling a rollover IRA into a 401(k) after year-end and assuming it changes the prior year’s conversion math.

Assuming different IRA accounts are separate buckets. For pro-rata purposes, they are not.

Common questions

Is the backdoor Roth IRA legal?

It is widely used and allowed under current rules. You are making a permitted Traditional IRA contribution and then doing a permitted Roth conversion. The key is reporting it correctly.

What about the step-transaction rule?

You might see people debate whether the IRS could apply the “step-transaction doctrine” to a quick contribution-then-conversion. In real life, the backdoor Roth is commonly done this way, and it is generally considered low risk when properly reported. If you want an extra-conservative approach, a tax pro can help you decide what you are comfortable with.

Will I owe taxes if I convert quickly?

If you have no other pre-tax IRA balances and your contribution was non-deductible, the taxable amount is often minimal. If you have other IRA balances, the pro-rata rule can create taxes even if you convert immediately.

What if I invested the Traditional IRA money before converting?

Not a disaster. Any gains that occur before conversion are typically taxable when converted. Losses reduce the value you convert. The bigger issue is still pro-rata, not a few dollars of growth.

Simple checklist

Confirm you are above the Roth IRA income limit for direct contributions.

Confirm the current year’s IRA contribution limit (and catch-up rules if you are eligible).

Check your year-end balances in Traditional, SEP, and SIMPLE IRAs.

Decide whether you can and want to move pre-tax IRA money into a 401(k) to avoid pro-rata issues.

Make a non-deductible Traditional IRA contribution (for the correct tax year).

Convert to Roth IRA (and remember conversions are reported in the calendar year they happen).

Verify Form 8606 is filed and accurate.

Final word

A backdoor Roth IRA can be a great tool for higher earners who want Roth growth and cannot contribute directly. But it is not “set it and forget it,” especially if you have existing pre-tax IRA money.

If you remember just one thing, make it this: the pro-rata rule is the difference between a clean backdoor Roth and a surprise tax bill.

This article is for educational purposes and is not personalized tax advice. If you are unsure how the pro-rata rule applies to you or how to file Form 8606, consider working with a qualified tax professional.