If you are trying to build credit as a couple, help a teenager start a credit history, or just simplify household spending, you will run into two similar sounding options: adding someone as an authorized user or opening a joint credit card account.

They can both put the same card in two wallets, but they do not come with the same credit reporting rules, legal responsibility, or exit plan. This is one of those decisions that feels small until it goes sideways.

Quick definitions

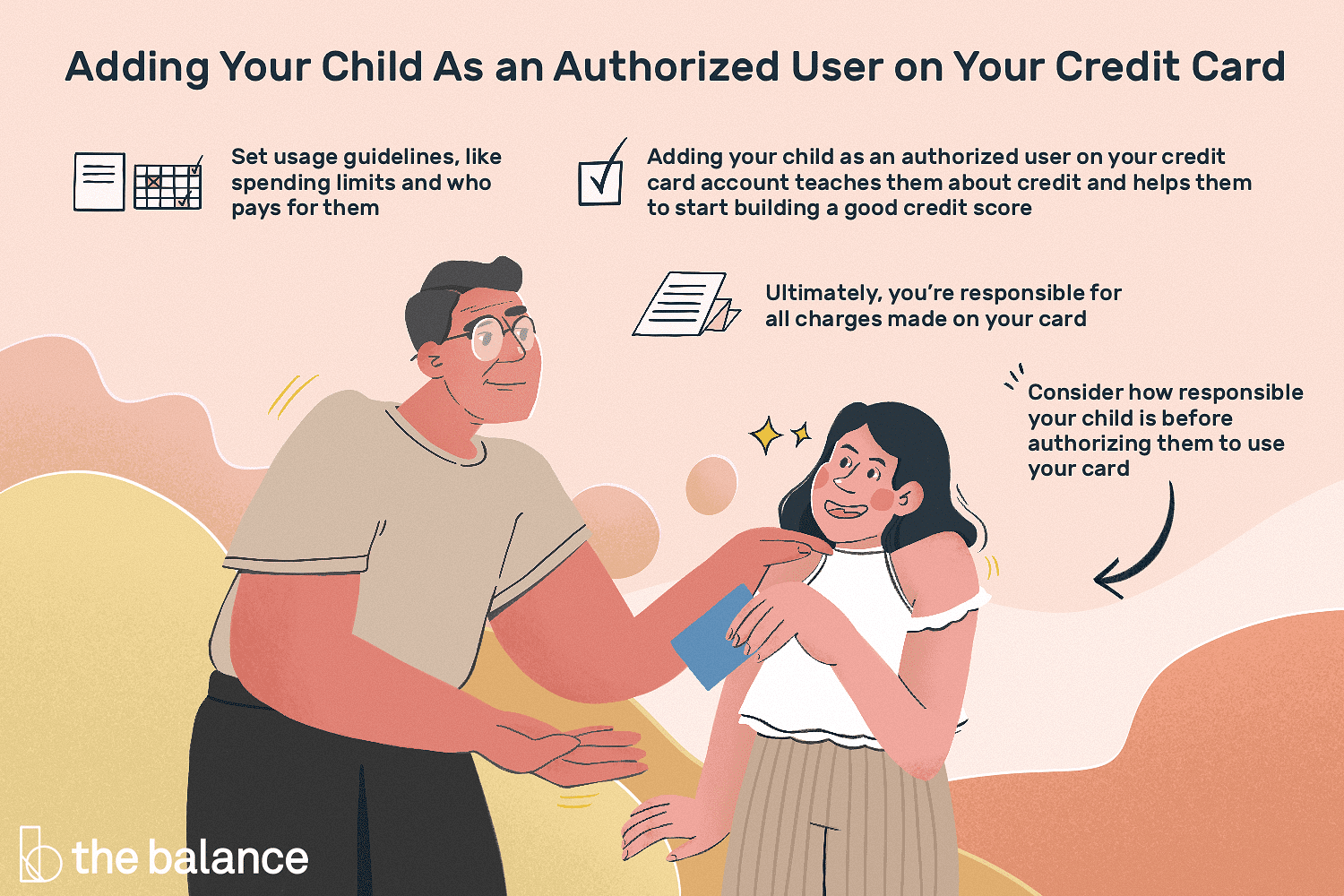

Authorized user

An authorized user is someone the primary cardholder adds to their existing credit card account. The authorized user gets their own card and can typically make purchases, but the account legally belongs to the primary cardholder.

Joint credit card account

A joint credit card account is a single credit card account with two co-owners. Both people apply, both are approved, and both are legally responsible for the balance.

Note: In the U.S., joint credit cards are less common today because many issuers stopped offering new joint applications. Some existing joint accounts are still out there, and availability varies by issuer and country.

Credit reporting

Here is the big credit building question: will the account show up on the other person’s credit report, and will it affect their score?

Authorized user reporting

- Often reports, but not always. Many major issuers report authorized user accounts to the credit bureaus, but policies vary and can change. Some issuers report limited details, and some do not report authorized users at all.

- If it reports, it can help or hurt. The authorized user may have the account’s age, credit limit, balance, and payment history reflected on their credit report.

- Impact is not guaranteed. Even if an authorized user tradeline appears on a credit report, some lenders and some scoring approaches may give it less weight or ignore it when making decisions.

- Some scoring models try to spot “piggybacking.” Modern models may reduce the impact in some cases, especially when the relationship looks like score-boosting rather than genuine shared household use. At the same time, authorized user accounts can still matter a lot for someone with a thin credit file, depending on the lender and the scoring version used.

Joint account reporting

- Typically reports fully to both people. Since both are owners, the account is generally treated like each person opened it themselves.

- Payment history is shared. One missed payment can damage both credit reports.

Practical takeaway: If your main goal is to help someone build credit with minimal long-term entanglement, authorized user status is usually the cleaner tool. If your goal is shared ownership of a revolving credit line, joint is the stronger commitment.

Legal responsibility

This is where people get surprised, especially in relationships.

Authorized user responsibility

- Primary cardholder is responsible for the bill. If the authorized user runs up charges, the issuer expects the primary cardholder to pay.

- Authorized users are typically not legally liable to the issuer for repayment. In most setups, the primary cardholder is the one on the hook. Still, cardmember agreements vary and you should assume the issuer’s contract controls.

- You may be able to set limits, but do not count on it. Some issuers allow spending limits or controls per authorized user, many do not, and enforcement can be imperfect.

Joint account responsibility

- Both co-owners are fully liable. This is “joint and several liability” in practice: the issuer can pursue either one for the full balance.

- Divorce or breakups do not change the contract. Even if a court order says one person must pay, the card issuer can still come after the other if payments stop.

Bottom line: If you would not comfortably cosign a loan for this person, a joint credit card is usually a no.

Undoing it later

When everything is going well, either option feels fine. The difference shows up when you need an exit.

Removing an authorized user

- Usually simple. The primary cardholder can typically remove an authorized user by calling the issuer or clicking a button online.

- Credit report updates take time. After removal, the authorized user tradeline may drop off their credit report on the next reporting cycle. In practice, it can take anywhere from a few weeks to 30 to 60+ days depending on issuer reporting cadence and bureau updates.

- Cleanest fix: remove first, dispute second. If the authorized user is still active at the issuer, the tradeline can keep reporting and can even reappear. Remove the authorized user with the issuer first, then dispute with the credit bureaus if it continues reporting incorrectly after that.

Removing yourself from a joint account

- Often hard or impossible without closing the account. Many issuers do not allow you to “un-joint” a joint credit card.

- You may have to close the account. That can affect both people’s utilization and account age, and it can create a short-term score drop.

- Balance transfers and payoff plans matter. If the account has a balance, you will need a plan before closing, such as paying it off or transferring it to an individual account.

My simple way to think about it: Authorized user is a light switch. Joint is closer to hardwiring.

Fraud and relationship risks

Credit cards are not like joint checking accounts. With cards, the issuer rules and fraud policies can get very specific, and credit score side effects can linger.

Authorized user risk points

- Spending risk. If the authorized user overspends, it is your balance and your utilization.

- Dispute and access limits. Authorized users may have limited power to dispute charges or get account details, depending on the issuer. Some issuers also limit what an authorized user can see or do online.

- Credit score whiplash. If the authorized user relies on the account for their score, removal can drop their score if they have a thin file.

Joint account risk points

- One person can wreck both scores. Late payments and high balances hit both reports.

- Harder to separate after conflict. If communication breaks down, joint accounts can become extremely difficult to unwind without cooperation.

- Death or incapacity can freeze things fast. Issuers often restrict, freeze, or close an account once they are notified of a death. Authorized user cards tied to that account may stop working, and joint accounts can still require coordination with the issuer and the estate process. Policies vary, so ask what the issuer does in these situations.

Credit building impact

If you are doing this for credit building, here is the simple way I think about it.

Authorized user is best when

- You are helping a teen or young adult build early credit history.

- You want them to benefit from your strong payment history and low utilization.

- You want an easy off-ramp if anything changes.

Joint account is best when

- You truly want shared ownership and shared responsibility for a household credit line.

- Both people have stable income, solid communication, and aligned spending habits.

- You are comfortable with the fact that either person can create debt the other must pay.

Two score mechanics to watch either way

- Utilization. High balances relative to the credit limit can lower scores fast, even if you pay on time.

- Payment history. One 30-day late can hang around for years.

Rule of thumb: If the goal is credit building, keep it boring. Low utilization, autopay on, and one clear person “in charge” of payment.

Alternatives that work today

Because joint credit cards are rare in many places, most people end up using one of these options instead.

- Primary + authorized user (with a shared routine). One person owns the account, both can use it, and you set autopay plus clear rules for spending and repayment.

- Separate cards + shared budget tool. Each person keeps their own card (and credit history), then you use a shared budget app or spreadsheet to settle up household categories.

- Add an authorized user for credit only. You can add someone as an authorized user and choose not to hand over the physical card. Depending on the issuer, you may also be able to limit the authorized user’s online access or freeze their card.

- For teens: secured or student cards. If the goal is credit building without relying on someone else’s account, a secured card or student card can be a cleaner long-term path.

Step-by-step: add an authorized user safely

- Pick the right card. Choose a card with a long positive history and low balance.

- Confirm the issuer reports authorized users. A quick call or secure message can save months of wasted effort.

- Turn on autopay for at least the minimum payment. This is non-negotiable if you are sharing access.

- Decide card access. You can add someone as an authorized user but keep the physical card locked away if your goal is credit history only. Also check whether the issuer lets you restrict what the authorized user can see or do online.

- Set expectations. Who can spend, what categories, spending caps, and how payback works.

- Monitor the account. Alerts for large purchases and payment due dates are your friend.

Step-by-step: consider a joint card

Because joint cards are not offered everywhere, you might be looking at an existing account or a rare issuer that still allows it. Either way, go slow.

- Ask the issuer how it works. Get clarity on liability and whether either party can request credit limit increases, add authorized users, or change account settings.

- Agree on a payoff plan. Decide how balances will be paid and what happens if one person cannot pay.

- Put your spending rules in writing. Not for romance, for clarity.

- Create an exit plan now. Will you close it, refinance with a balance transfer, or move charges to separate cards if you split?

At a glance

- Credit reporting: Authorized user often reports (details and impact vary); joint usually reports to both as owners.

- Who owes the debt: Authorized user, primary cardholder; joint, both people fully.

- How easy to undo: Authorized user easy; joint often requires closing or issuer cooperation.

- Best for: Authorized user for credit building and controlled access; joint for true shared household responsibility.

FAQs

Is an authorized user the same as a joint account?

No. Authorized users are added to someone else’s account. Joint account holders are co-owners who are both responsible for the debt.

Can being an authorized user hurt my credit?

Yes. If the primary cardholder carries a high balance, misses payments, or the card is maxed out, that negative information can be reported on the authorized user’s credit report too. Also, some lenders may discount authorized user lines even if they appear, so do not treat this as a guaranteed score boost.

Can I remove myself as an authorized user?

Often yes. You can ask the primary cardholder to remove you, and many issuers will also let the authorized user request removal. If the account keeps reporting after the issuer confirms you are removed, you can dispute it with the credit bureaus.

Is a joint credit card a good idea for married couples?

Sometimes, but it is rarely necessary. Many couples get the same convenience with one primary cardholder and one authorized user, plus clearer responsibility and an easier exit if life changes.

My bottom line

If you want the simplest way to help someone build credit with limited long-term risk, authorized user usually wins. If you want true shared ownership and you are comfortable being fully responsible for the other person’s charges, a joint credit card can work, but you need crystal-clear rules and a realistic exit plan.

Money stress loves gray areas. Your goal here is to make the arrangement painfully clear while things are still good.

Important: This is general information. Issuer policies, reporting practices, and lender scoring can vary.