I still remember the stomach-drop feeling of checking my balances and realizing my “normal” payment schedule would keep me tethered to debt for years. Student loans can feel like that for a lot of us: you pay every month, but the finish line barely moves.

The good news is you do not need a miracle. You need a handful of proven tactics that lower interest, increase how much hits your balance, and reduce the number of days your loans have to rack up interest. Below are seven strategies I’ve seen work in real life, and you can mix and match them.

1) Pick the right repayment plan first

Before you throw extra money at your loans, make sure your repayment plan matches your goal.

Federal loans: optimize for the right outcome

- Paying off ASAP: A standard 10-year plan is often the fastest “set it and forget it” option among common federal choices. If your income allows, you can still pay extra on top of it.

- Lower required payment: Income-driven repayment (IDR) can free up cash flow. That can help you avoid missed payments and may give you room to make targeted extra payments. Just know some IDR plans can extend repayment and increase total interest if you only pay the minimum.

- Public Service Loan Forgiveness (PSLF): If you are genuinely on track for PSLF, “faster payoff” might not be the best goal. The best strategy could be minimizing payments while staying compliant to maximize forgiveness. In general, extra payments do not increase forgiveness value if you are pursuing PSLF.

Quick win: Write down your actual goal in one sentence: “I want to be debt-free by ___” or “I want PSLF forgiveness and the lowest total out-of-pocket cost.” Your strategy should match that sentence.

Safety note: Aggressive payoff is great, but try not to do it at the expense of a basic emergency fund. Even a small cash buffer can keep one surprise expense from turning into new high-interest debt.

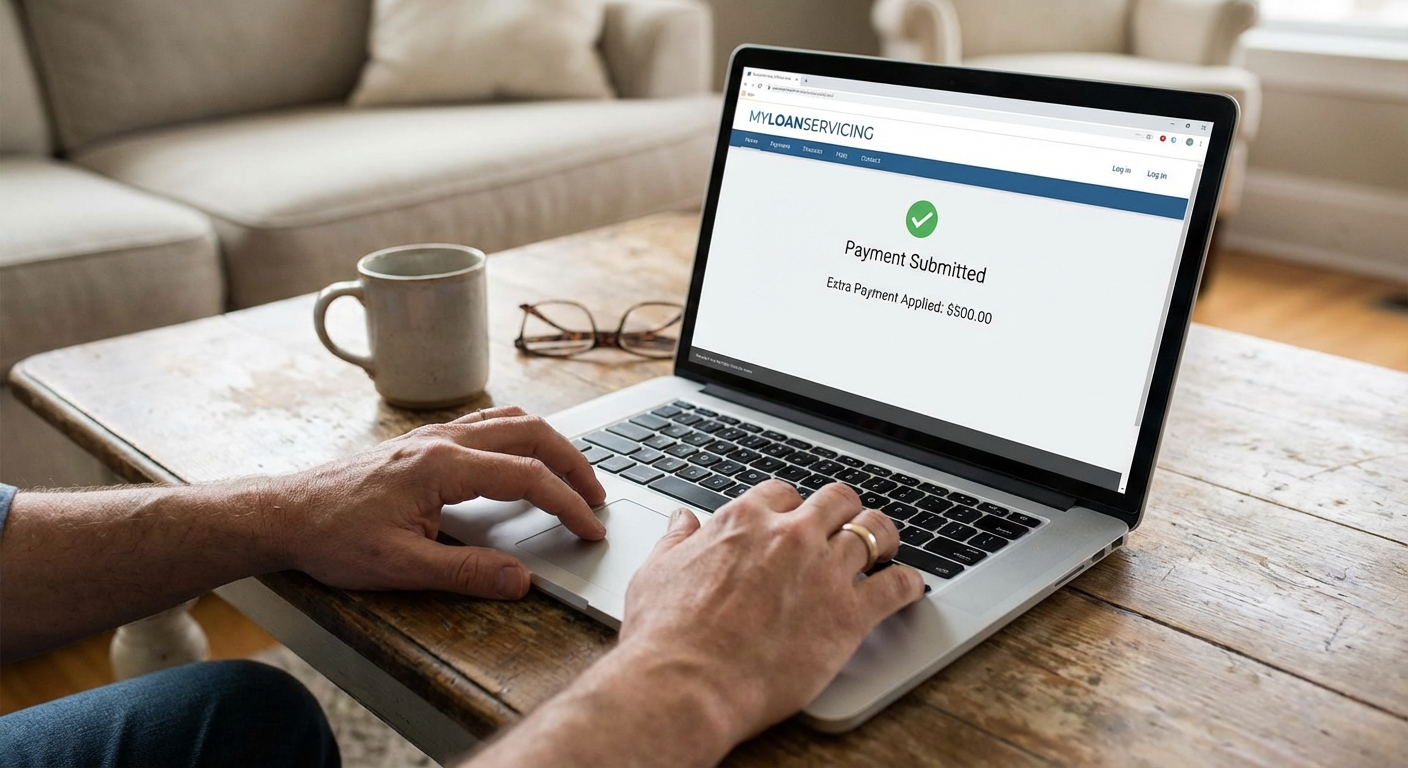

2) Make extra payments correctly

This is where people lose momentum. You can send “extra,” but you want it credited in a way that actually reduces what you owe and keeps your next bill on schedule.

How extra payments really get applied

- Interest first is normal: Servicers typically apply payments to any accrued interest and fees first, then to principal. That is not a rip-off, it is just how loan accounting works.

- Avoid “paid ahead” confusion: The bigger issue is often whether your servicer advances your due date (puts you in “paid ahead” status) instead of keeping your next payment due as scheduled. If you want faster payoff, you usually want the extra treated as an additional payment toward your current balance, not as a future month’s payment.

- Target a specific loan: If you have multiple loans, choose the specific loan group for your extra amount. This is especially important if you are using avalanche or snowball.

- Autopay plus a separate extra: Keep autopay for the minimum payment and send a separate “extra” payment. It makes tracking easier and helps prevent accidental underpayment.

My favorite simple approach: Minimum payments on everything, then one extra payment each month targeted to a single loan (we’ll pick which loan in the next strategy).

Also worth checking: Many servicers offer a small interest rate discount for enrolling in autopay. It is not life-changing, but it is a free win if it fits your cash flow.

3) Use avalanche to pay less interest

If your goal is to pay off faster and pay less overall, the debt avalanche is the math-forward move.

- List your loans by interest rate, highest to lowest.

- Pay the minimum on all loans.

- Send every extra dollar to the highest-interest loan until it is gone.

- Roll that payment into the next highest rate loan.

This works especially well if you have a mix of rates, like older federal loans at 6.8% and newer ones at lower rates, or private loans with higher APRs.

If motivation is your biggest challenge: The snowball method (smallest balance first) can be easier emotionally. Paying faster is partly math and partly psychology. Pick the method you will stick with for the next 12 months.

4) Pay more often (biweekly or recurring extra)

One of the easiest ways to accelerate payoff is to make payments more frequently.

Two ways to do this safely

- True biweekly: Pay half your monthly payment every two weeks. If you complete all 26 half-payments, that equals 13 full payments per year instead of 12.

- Weekly mini payment: You can divide your monthly payment by 4 and pay that amount weekly to smooth cash flow. Just know this does not reliably create a 13th payment, because some months effectively have more than 4 weeks.

Why it can help: The biggest benefit is the extra annual payment (with true biweekly). There can also be a small interest benefit from paying earlier since student loan interest accrues daily, but the impact varies.

Important: Not every servicer handles partial payments cleanly. If your servicer is messy about partial payments, keep autopay for the normal monthly payment and set a separate recurring extra payment equal to your monthly payment divided by 12. That approach reliably creates the “13th payment” effect over a year.

5) Refinance strategically

Refinancing can be a rocket booster, but only when it fits your situation.

When refinancing can help

- You have private student loans with a high interest rate.

- You have strong credit (or a cosigner) and stable income.

- You want a lower rate, a shorter term, or both.

When to be cautious

- Federal loans: Refinancing federal loans into a private loan means you give up federal protections like IDR plans, PSLF eligibility, deferment options, and certain hardship protections.

- Variable rates: A variable rate can rise later, which can undo your progress.

My “refinance test”: If you can lock a meaningfully lower fixed rate and you are not relying on federal benefits, refinancing can reduce interest and speed up payoff. If you might need federal flexibility, consider other strategies first.

Two quick checks: Shop multiple quotes, and confirm there is no prepayment penalty (they are uncommon, but worth verifying).

6) Automate a payment bump

This one is boring. It is also ridiculously effective.

Each time you get a raise, a new job, or pay off another debt, increase your student loan payment by a set amount. Even a small bump makes a huge difference over time because it reduces your balance earlier.

Make it automatic with a simple rule

- Raise rule: Put 50% of every take-home pay increase toward loans until you hit your target payoff timeline.

- Debt swap rule: When a car loan or credit card is paid off, roll that exact payment into your student loans.

- Annual review: Once a year, recalculate your payoff date and adjust the bump.

Value-spender tip: You do not have to send 100% of extra income to debt. Build a plan that lets you live your life and still win the math.

7) Use outside money

To pay off student loans faster without feeling squeezed, the best dollars are the ones that do not come from your grocery budget.

Employer student loan help

Some employers contribute monthly toward your student loans as a benefit. Ask HR if they offer a student loan repayment program or educational assistance benefits. If they do, set up payments so the money goes straight to the loan you are targeting (like your highest-interest loan).

Also worth asking about: Under the SECURE 2.0 Act, some employers can treat your student loan payments like elective deferrals for retirement matching purposes. That means you may be able to get an employer match in your 401(k) or similar plan even if your cash is going to student loans.

Tax moves that can free up cash flow

- Student loan interest deduction: If you qualify, this can reduce your taxable income and increase your refund or lower your tax bill. Income limits apply, and higher earners are phased out.

- Refund strategy: If you consistently get a big refund, consider adjusting withholding so you keep more money each paycheck, then automate that amount to your loans.

Verification note: Tax rules and employer benefit rules can change. Verify current IRS guidance and your employer plan terms before you build your whole strategy around them.

A realistic side hustle plan

You do not need a second full-time job. Even $200 to $400 per month can speed up payoff meaningfully, especially when targeted at high-interest loans. Think: weekend gig work, freelancing a skill you already have, selling unused items, or a seasonal hustle you can stop when burnout hits.

A payoff plan for this week

If you want a clean starting point, here is a no-overwhelm setup:

- Pick your target loan: Highest interest rate (avalanche) or smallest balance (snowball).

- Turn on autopay for the minimum payment on all loans (and capture any autopay discount if offered).

- Schedule one extra payment each month to your target loan, even if it is only $25.

- Add one accelerator: Either true biweekly payments or a refinance quote (if you have private loans).

- Set one calendar reminder for a quarterly check-in to increase your extra payment if you can.

Small steps stack up fast, especially when your extra dollars are consistently hitting your current balance and you keep your due dates on track.

Heads up: Student loan rules and repayment options can change, and your best strategy depends on whether your loans are federal or private. If you are pursuing PSLF or relying on income-driven repayment, double-check how extra payments, consolidation, and refinancing could affect your benefits. If you are on IDR, build a reminder to recertify on time and periodically confirm your qualifying payment count if PSLF is your goal.

FAQ

Is it better to pay off student loans faster or invest?

It depends on your interest rate and your stress level. If your loans are high-interest, paying them down faster is often a strong guaranteed “return.” If your rate is low and you are already saving for retirement, you may choose a balanced approach: invest consistently while making targeted extra payments.

Should I pay extra on federal student loans?

You can, but first confirm you are not better served by a forgiveness path (like PSLF) or by keeping flexibility through an IDR plan. If forgiveness is not in the picture and your emergency fund is in decent shape, extra payments can absolutely help.

Do biweekly payments always reduce interest?

They can, mainly because true biweekly payments create one extra payment per year if you complete all 26 half-payments. Paying earlier can also reduce interest slightly since interest accrues daily. The key is making sure your servicer credits payments the way you expect and does not simply push your due date forward.

Bottom line

You do not need to do all seven strategies to make real progress. Pick two or three that fit your life and run them for 90 days. Your payoff date will start moving, your anxiety will drop, and you will feel that momentum that makes the rest of the journey way easier.